PakAlumni Worldwide: The Global Social Network

The Global Social Network

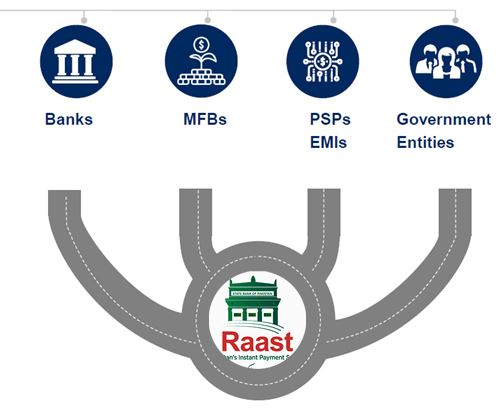

Raast Aims to Create Pakistan's Unified Digital Payments Infrastructure

Pakistan's central bankers have taken the plunge into the world of digital payments with their own offering: Raast. It aims to create an instant low-cost payment system that can seamlessly and securely connect government entities, a variety of banks, including microfinance banks (MFBs), electronic money institutions (EMIs) and State Bank authorized payment service providers (PSPs) like 1Link and NIFT which may choose to take advantage of it. Currency and coins in circulation account for about 43% of Pakistan's total money supply. The introduction of Raast is part of the government's effort to modernize and document the nation's cash-based informal economy. Undocumented economy poses a serious threat to the country because it creates opportunities for criminal activities and tax evasion. Digital financial services will also promote e-commerce in Pakistan.

|

| Raast Digital Payment System. Source: State Bank of Pakistan |

Raast Digital Payments:

Raast is a system of digital payment infrastructure. It is essentially a pipe that is intended to connect government and financial institutions with consumers and merchants with each other to process payments instantly at very low cost.

Raast will be boosted by Pakistan government's decision to use it to pay salaries, pensions and pay welfare recipients under Benazir Income Support and Ehsaas Emergency Cash programs.

State Bank of Pakistan intends to demonstrate Raast's usefulness by first processing government payments to individuals, including government employees and Ehsaas welfare beneficiaries, before expanding it for business applications. SBP’s plan is to start person-to-person (P2P) payments using just the phone numbers in Q3/2021 and then bring merchants on board with QR codes by Q1/2022.

Pakistan's Sadia Zahidi Leads WEF Gender Equity Effort

Brothers From Rural Pakistan Teaching AI to American High Schoolers

Pakistan's Computer Services Exports Jump 26% Amid Coronavirus Lock...

Pakistan Gig Economy Among World's Fastest Growing

Digital BRI and 5G in Pakistan

Pakistan's Demographic Dividend

Pakistan EdTech and FinTech Startups

State Bank Targets Fully Digital Economy in Pakistan

Campaign of Fear Against CPEC

Fintech Revolution in Pakistan

E-Commerce in Pakistan

The Other 99% of the Pakistan Story

FMCG Boom in Pakistan

Belt Road Forum 2019

Fiber Network Growth in Pakistan

Riaz Haq's Youtube Channel

Views: 958

-

Comment by Riaz Haq on February 11, 2021 at 10:21am

-

SBP, after approval of the Federal Government, has introduced three new categories of investment abroad under its revised policy governing equity investment abroad and banks have been authorized to allow remittances under newly introduced categories.

https://propakistani.pk/2021/02/10/sbp-modernizes-foreign-exchange-...

1. Establishment of Holding Company abroad by residents for raising capital from abroad: Pakistan’s investment regime is quite liberal that allows full freedom to repatriate profit, dividend, and capital. However, some international investors prefer to invest indirectly through a holding company established abroad specially in the Fintech and Startup firms. SBP’s revised policy will enable the Pakistani Fintech and startup companies to channelize foreign direct investment in the country by establishing a holding company abroad against remittance of up to USD 10,000 and subsequent swapping of shares to mirror the shareholding of a local company in the holding company.

2. Establishment of subsidiary/branch office abroad by export-oriented companies/firms for promoting exports: The policy will enable the export-oriented companies to establish subsidiary/branch office abroad against remittance of 10 percent of their average annual export earnings of last three calendar years, or USD 100,000 whichever is higher. This will facilitate exploring new and non-traditional markets and capturing more export orders, as international buyers prefer dealing with subsidiaries/representative offices of foreign companies present in their country. Accordingly, the proposed policy would help in the growth of export-oriented companies and boost the exports of the country.

3. Investment abroad by Resident Individuals: The policy will allow the Resident Individuals of Pakistan to acquire an equity stake in international firms through share option plans or investment in listed securities subject to observance of the annual ceiling of foreign exchange defined in the policy. In the case of sweat equity, a person can acquire up to twenty percent shareholding in a foreign company. These policy provisions will provide opportunities to individuals to earn foreign exchange for the country in the form of repatriation of dividend/ capital gains to Pakistan.

-

-

#Unilever’s #Pakistan #Delivery Service Partner blueEX Plans #IPO on #KSE to Expand Network. #Karachi-based courier service plans to sell new shares equal to 25% of the company within the next two months. #ecommerce #economy #tech https://www.bloomberg.com/news/articles/2021-02-19/unilever-s-pakis...

Universal Network System Ltd., a Pakistan courier service that counts the local units of Unilever Plc and Nestle SA as clients, is planning an initial public offering to expand its network and bolster its technology backbone.

The Karachi-based company, which operates the blueEX courier service, plans to sell new shares equal to 25% of the company within the next two months, said Chief Executive Officer Imran Baxamoosa. He didn’t disclose financial details.

The initial share sale will make it the first logistics company to list in Pakistan and lure investors to a business that’s crucial for the nation’s booming e-commerce industry, according to Topline Securities Pakistan Ltd., financial adviser for the IPO.

“There is some crazy exponential growth that is being foreseen right now,” Baxamoosa said in a phone interview. “We have grown organically so far but now it’s about time that we get aggressive.”

The courier company that started by handling cargo in 2005 entered the e-commerce business six years later by going door-to-door and convincing companies to start online sales. It even made websites, back-end software and set up a call center for its clients.

It now has about 1,000 employees and over 350 vehicles. The company will use the proceeds to boost its network fourfold. It will also add servers and other IT equipment.

The nation’s e-commerce industry is in its infancy but is growing rapidly as internet and smartphone penetration jump, according to Ruchir Desai, fund manager at Hong Kong-based Asia Frontier Capital Ltd. The pandemic could be a big trigger for the market, he said.

The company handled 2.1 million shipments and 4.5 billion rupees in cash deliveries in the year ended June. It has grown annually by about 70% on average since 2012. The company forecasts revenue will rise more than three times to 4.3 billion rupees in fiscal 2023, according to Baxamoosa.

-

-

China’s new digital yuan: Lessons for Pakistan

https://dailytimes.com.pk/719831/chinas-new-digital-yuan-lessons-fo...

Muhammad Zubair Mumtaz

FEBRUARY 3, 2021

As more and more nation contributes to and depend on the global economy, the process associated with routing payments smoothly so that they can be monitored by the central banks becomes important. Over time, various types of digital payments were introduced to facilitate business and household transactions. However, a lot more is required to be done by Central Banks to help build trust in digital payments.

China, being the leader, has launched a Central Bank Digital Currency (CBDC). An initiative was taken in September of 2020 to allow Digital Currency Electronic Payments (DC/EP). In simple words, the DC/EP is a digital version of the Chinese yuan backed by deposits held by the central bank. To take advantage of this form of digital payments, banks must replace a portion of yuan holdings with assets that are in digital form and then allocate it to businesses and the public using mobile technology.

In contrast, payments are also made using cryptocurrencies; what is different in DC/EP? The answer is the legal status that differentiates between DC/EP and cryptocurrencies. In terms of making payments through cryptocurrencies, the laws are vague in regards to whether it is legal to pay for goods and services in China using this form of payment; however, DC/EP is recognized as a legal tender to make transactions. The government will also control the digital yuan while cryptocurrencies are decentralized and do not have a single entity to manage their supply. Anonymity is another significant difference between the digital yuan and cryptocurrencies. Cryptocurrencies are anonymous whereas the digital yuan will be monitored, tracked, and backed by the government.

---------------

On January 11, 2021, Prime Minister, Imran Khan, launched the first digital payment system, ‘Raast,’ to promote financial inclusion and government revenue. This system will be implemented in three phases ending in early 2022. This timely initiative by the government is highly commendable as it will serve its purpose in many ways. Several private-sector digital cash transfer systems already exist that do not require a bank account like JazzCash, Easypaisa, Telenor Pakistan; however, Raast would be the first to connect government organizations and financial institutions. Businesses, fintechs, merchants, individuals, and government entities will utilize this system to receive and send real-time payments via the internet, mobiles, and agents. Using the Raast, the government will pay salaries, pensions, and financial support programs (e.g., the Benazir Income Support Program, the Ehsaas Emergency Cash program, etc.). This initiative is vital to restrict illegal financial transactions perpetuated by militant and extremist organizations. An essential requirement of the Financial Action Task Force (FATF) is fulfilled through digital payments which will help Pakistan come off of the grey list. Furthermore, Raast will automate the collection of taxes on transactions and tighten rules on banking.

Though Raast is not an alternative to digital currency it will be useful to align the transaction channels as the government will have full information about receipts and payments. Based on this information, the informal economy will be brought into the tax net and corruption can be reduced significantly. The government may also control the money supply and take fiscal and monetary measures accordingly.

-

-

Digital transactions boom in Pakistan

According to the (State Bank of Pakistan) report, during the Oct-Dec 2020 quarter, 296.7 million e-banking transactions, valuing at Rs21.4 trillion, were carried out, registering a growth of 24% in volumes and 22% in value compared to the same quarter of last year.

Most of the rise in e-banking transactions was seen in internet and mobile banking.

“Owing to Covid-19, it is no surprise that the country has seen a boom in digital financial transactions,” he said, adding that for most of the people before 2020, e-banking was a difficult process to handle, which carried with it significant security risks as well.

“Coronavirus lockdown was a forceful phenomenon, but it is now turning into a normal thing,” remarked DH Corporation Research Lead Karim Punjani.

The volume of mobile banking transactions stood at 44 million, up 147%, valuing at Rs1.12 trillion, up 192% in the quarter under review compared to 17.8 million transactions valuing at Rs382.5 billion in the same quarter of last year.

The number of registered mobile phone banking users reached 9.4 million, an increase of 5%. Similarly, 22 million internet banking transactions valuing at Rs1.3 trillion were recorded during the Oct-Dec 2020 quarter compared to transactions worth Rs1.1 trillion in the previous quarter.

“The decision taken by the central bank to waive inter-bank fund transfer (IBFT) charges is a good move and we hope this continues,” said Nouman Younas, who recently conducted online transactions.

“Decisions such as waiving the IBFT fee will lead to a reduction in the workforce in commercial banks,” said another digital transaction user Adeel Nazir.

In response to SBP’s measures to incentivise the installation of Point-of-Sale (POS) machines to facilitate digital payments through debit or credit cards, the number of POS machines grew 18% during the quarter under review, reaching 62,480 throughout the country, the report said.

With the help of these POS machines, 23 million transactions amounting to Rs115 billion were processed during the second quarter of FY21, which shows the positive impact of conducive policies adopted by the central bank, particularly targeted at increasing the payment acceptance infrastructure in the country.

Authorities should encourage banks to establish CDM (cheque/cash deposit machine) like ATMs as they eliminate human interaction and increase online banking efficiency, said a Karachi-based user of digital transactions Mubashir Mahmood.

Card-based transactions on e-commerce portals also increased substantially, with e-commerce merchants processing 5.6 million transactions through payment cards amounting to Rs15 billion in the second quarter of FY21 compared to 3.9 million valuing at Rs11.9 billion in the first quarter.

This marks a shift in the behaviour of Pakistan’s population and also complements government’s efforts to develop a more market-friendly landscape for acceptance of payments by e-commerce merchants.

-

-

#Pakistan #fintech SadaPay raises $7.2 million in country's largest seed round. #Islamabad-based fintech startup has raised $7.2 million in a seed round led by New York-based Recharge Capital. #technology #investment https://www.menabytes.com/sadapay-seed/ via @MENAbytes

It includes participation of returning investor Kingsway Capital, Raptor Group, and notable fintech angels, including Ualá’s founder Pierpaolo Barbieri, Ribbit Capital’s Brian McGrath, former General Catalyst partner Ilan Stern, and Valon Technologies’ founder Andrew Wang.

Starting with a digital wallet and a debit card, SadaPay aims to build a “neobank” for Pakistan. Currently available in private beta, its mobile wallet is one of the most anticipated fintech products in the country, with over 200,000 people on the waitlist. It launched the private beta a few months ago after receiving in-principle approval from the country’s central bank. In this pilot phase, SadaPay is allowed to operate with a maximum of 1,000 customers.

The startup will start its public rollout after receiving a full Electronic Money Institution license from the State Bank of Pakistan. SadaPay did not share a timeline, but its founder Brandon Timinsky has told MENAbytes that they would receive the license after successfully completing the audit and inspection from the regulator.

Brandon had started SadaPay in 2019 after selling his previous startup in the United States. He was visiting Pakistan on the invitation of a friend and was amazed by the opportunity that the country of over 220 million offered, “My first visit to Pakistan really opened my eyes to the amount of opportunity that has been hidden from the rest of the world due to the country’s difficult history from over a decade ago,” he stated in a conversation with MENAbytes.

As the statement by the company points out, Pakistan is the fifth most populous country in the world but has the third largest unbanked population after China and India. Brandon believes that the country is at an inflection point for digitization, “Pakistan has a refreshingly progressive regulator, a burgeoning unbanked middle class, widespread smartphone adoption, and over 70% of the population is under the age of 35. We believe that a combination of factors makes Pakistan one of the best places for emerging fintech in the world, and we are excited to be a leader in that ecosystem.”

SadaPay’s mobile app enables users to sign up for a mobile wallet account with a few taps in less than two minutes and start using it right away to make free transfers to any bank account in Pakistan. The signup process is seamless mainly because the company is connected to Pakistan’s National Database & Registration Authority (NADRA) – which means it can instantly verify any Pakistani’s identity from anywhere in the world, including the 15 million Pakistani expatriates living abroad.

The account comes with a virtual debit card powered by Mastercard that can be used for online transactions all around the world. SadaPay also offers a physical numberless debit card that the users can request from its app and receive at their doorstep in two business days (across Pakistan). The physical card allows users to make up to three free cash withdrawals (every month) from any ATM in Pakistan. The company also supports remittances from services like Transferwise, Remitly, and WorldRemit.

When launched, any overseas Pakistani will be able to sign up for a SadaPay account using their NADRA-issued ID card, the company’s CEO told MENAbytes, adding that will become the easiest way to send money to Pakistan, for free, at the best exchange rates in the world.

“Since SadaPay does not bear the high costs of managing the physical infrastructure of traditional banks, it passes those savings to its customers in the form of free financial services. The company will generate revenues from premium product offerings such as merchant services and remittances,” noted the statement.

-

-

India has the highest percentage of smartphone users, at 69 percent, followed by Sri Lanka with 60 percent, Nepal 53 percent and Pakistan 51 percent.

https://www.thedailystar.net/backpage/news/bangladesh-behind-nepal-...

The report was unveiled at a virtual roundtable organised jointly by GSMA (Groupe Spécial Mobile Association) and the Association of Mobile Telecom Operators of Bangladesh (AMTOB).

The report, titled "Achieving mobile-enabled digital inclusion in Bangladesh", said 4G network now covered 95 per cent of the population. Yet, there was still a significant usage gap of 67 per cent as only 28 per cent of the population had 4G connections.

"This suggests a lag between 4G coverage rollout and usage of 4G services. This lag in usage is largely explained by issues related to the affordability of devices, low levels of knowledge and digital skills, a perceived lack of relevance, as well as safety and security concerns."

High sector-specific taxes, a fragmented licensing regime, as well as issues with the pricing and usage restrictions on spectrum have been identified as barriers to expanding coverage.

Bangladesh, however, fares better compared to Nepal and Sri Lanka in terms of 4G connections. Only 17 per cent of the population has 4G connections in Nepal, and 18 per cent in Sri Lanka, according to the report.

India has the highest 4G connections at 63 percent of the population followed by Pakistan.

Bangladesh has 17 crore mobile connections. Of them, nine crore are unique subscribers, giving a penetration rate of 54 percent as of December 2020.

Some 47 percent of subscribers use 2G connections and 25 per cent 3G connections.

The report said internet and digital technology played a key role in helping drive economic growth and societal development in Bangladesh.

Digital technologies, mobile in particular, will be crucial to implementing the government's 2041 Perspective Plan, achieving the Sustainable Development Goals, and recovering economically in the aftermath of the Covid-19 pandemic, the report said.

-

-

Pakistan ready to adopt digital financial solutions on large scale, says Easypaisa CEO

“Pakistan is rapidly progressing when it comes to mobile broadband. Our country has enormous potential with respect to widening financial inclusion through digital solutions. Currently, 95 million people across the country use mobile broadband, a number which has grown by 50 million in the past 5 years. A majority of adults have broadband connections in Pakistan serving as a backbone to developing a digital payments ecosystem in the country.” said M. Mudassar Aqil, CEO Easypaisa/Telenor Microfinance Bank, while talking about Pakistan’s financial services landscape.

“96% individuals have a biometrically verifiable ID issued by the government, indicating that a robust regulatory framework is in place which is supported by credit bureaus. Despite these fundamental factors, 70% of Pakistanis don’t have access to financial services when the rails to address these challenges are in place,” he added. During COVID-19, digital payments witnessed a boom. According to the SBP’s quarterly report, 296.7 million e-banking transactions, valuing at PKR21.4 trillion, were carried out during Oct – Dec 2020, growing by 24% in volume and 22% in value compared to the same quarter last year.

“During COVID-19 industry numbers of digital transactions grew at an exponential rate. At Easypaisa, our annual throughput increased by 64% as compared to the previous year reaching PKR 1.5 trillion in 2020. Similarly, the number of active Easypaisa App users reached 3.44 million, registering a 54% increase in comparison to previous year.” he commented. Pakistan is predominantly a cash-based economy. However, things are changing as the use of digital payments is taking center-stage.

Mudassar opined: “The Pakistani economy is ready to adopt digital financial solutions on a large scale as opening a mobile wallet account on a smartphone or feature phone takes less than a minute. Roughly PKR 6 trillion or about one-third of the country’s deposits are in circulation. This is one of the highest percentages anywhere in the world and the only way to reduce this is for every adult in the country to have a mobile wallet. Furthermore, all retail outlets in Pakistan should be mandated by law to accept digital payments from mobile wallets. Tax incentives should also be introduced making digital payments cheaper than cash.”

-

-

Pakistan: Central Depository Company (CDC) and National Institutional Facilitation Technologies (NIFT) signed an agreement to enable digital payments through NIFT ePay.

https://nation.com.pk/08-Apr-2021/cdc-signs-agreement-with-nift-to-...

CDC is recognised as the infrastructure backbone of Pakistan’s capital market and it is the sole securities depository in the country, while NIFT is one of the largest payment processors in Pakistan.

This collaboration will enable the investors to use NIFT ePay services for investing into Mutual Funds using CDC’s digital platform” “Emlaak Financials.” Furthermore, the solution will also be facilitating CDC’s IAS account holders to make IAS payments through CDC Access portal.

The agreement was signed by NIFT’s CEO Haider Wahab, and CDC’s CEO Badiuddin Akber at the CDC’s head office.

NIFT’s CEO stated, “We are delighted to be a part of CDC’s newly launched initiative for the Mutual Fund Industry. We understand that the “Emlaak Financials” platform has an aspiring roadmap, and we look forward to playing our role in enabling the platform and in making this service a success. NIFT will always focus to partner for unique and innovative ideas which will uplift the digital transformation in Pakistan.”

At the signing ceremony, CDC’s CEO Badiuddin Akber said, “As we embark on this collaboration with NIFT, it gives us immense pride that we are engaging NIFT’s payment gateway for the first of its kind mutual fund aggregator platform , being launched in the financial landscape of Pakistan. The launch of this platform and its integration with NIFT’s services to enable secure and swift payments for mutual fund investors is in-line with CDC’s vision of enhancing efficiency and ease of doing business.”

-

-

#Pakistani-#American founder's #SiliconValley payment processing company i2c vows to hire 500 employees in Pakistan as it continues to grow at exponential rate. The #fintech has 65% of its workforce based in #Lahore, #Pakistan. #technology

https://www.techjuice.pk/i2c-hire-500-people-pakistan/

i2c has recently hired Jon-Paul Ales-Barnicoat to lead its human resources development as the organization plans to massively scale and hire 500 resources in the next 12 months majorly from Pakistan making the total organizational headcount to over 2500.

Jon Paul is an industry veteran with experience of working at Silicon Valley tech companies including Fandom, Pixar, GE. Joining i2c is a new experience because the company is majorly driven by the workforce in Pakistan and most of the human capital too is based here. With the ongoing conversation about the future of remote work, we felt it would be interesting to understand Jon Paul, the new Chief Human Resource Officer’s perspective and how he visualizes that for i2c, given the organization has been working remotely before the rise of the term ‘future of work’ and ‘remote working’.

So, we sat with Jon Paul during his recent visit to Pakistan to discuss the tech ecosystem, i2c, and how the organization plans on scaling effectively right from the heart of Pakistan, Lahore.

Founded in 2001, and headquartered in Silicon Valley, i2c’s next-generation technology supports millions of users in more than 200 countries and territories. It is a common name in the tech circles of Pakistan. Specially fresh graduates in Computer Sciences, Software Engineering and other IT related fields are aware of the organization because of its large scale hiring drives in the north and center of Pakistan.

Jon tells me how he is excited to be visiting Pakistan for the first time and working from i2c’s Lahore office. I ask about how his experience has been so far. Jon tells me, “Pakistani people in particular have been very welcoming and sincere in their intention. The value system is very precious. The sense of community, and the family values are permeated into professional relationships as well. And there’s a tremendous amount of loyalty and respect for one another.” I was curious how i2c is unlocking that value system in the workplace.

Jon tells me,

“You see i2c is built on the shoulders of Pakistani employees. We understand their contributions and provide benefits which are very nurturing for our employees.

We give our employees cars. We have a daycare center. We feed our employees twice a day. Our medical benefits are amazing. And we have education benefits for our employees’ children. And now we have created a real cash plan where our employees are going to get a share in the success of the company. We contribute to the retirement fund as well. Very few companies of our size do that.”

i2c has been quietly setting its foot in different regions of the world. Right now the Pakistani offices have almost 1000 employees in total whereas outside the country, there are over 600 employees based in US, Canada, Europe, Latin America. The organization will be expanding across all regions with specific plans to hire over 500 employees in Pakistan in the next 12 months. I was curious if there is a process for rotational assignments, and internal transfer of employees between different countries. Jon told me that Amir, the founder, and he have been working on it and believe that this is a great differentiator and advantage for their employee base in Pakistan. Due to COVID situations, this program is on halt but there have been several examples of employees moving from Pakistan to the US and later to Canada.

-

-

SBP launches free P2P fund transfers under Raast

https://www.dawn.com/news/1673190

The State Bank of Pakistan (SBP) on Thursday directed banks to introduce free person-to-person (P2P) fund transfers under Raast, a digital payment system.

The central bank said it has issued instructions to banks that will enable P2P payments in the country through Raast.

The central bank has been working hard for reforms in the financial system through digitisation and improvement in the payment system. Several measures were taken to bring the payment system on a fast track with minimum time spent.

Developed by the SBP, Raast — an Urdu word that means correct and direct — offers an instant, reliable and zero-cost digital payment system to the people of Pakistan.

The SBP believes that the launch of Raast P2P service will not only provide a convenient and hassle-free digital fund transfer service to customers but will also provide an efficient and enabling payments infrastructure that would pave the way for digitisation of the economy and promotion of digital financial services in the country.

The SBP has provided an explanatory video on YouTube and SBP’s website that explains to the public in simple terms how to make payments and transfer funds using Raast.

“Under Raast P2P fund transfers and settlement services, bank customers would be able to send and receive funds in their accounts using their bank’s mobile application, internet banking, or over-the-counter services,” said the SBP.

For customers’ facilitation, they can set their registered mobile phone number as their Raast ID and link it to their preferred International Bank Account Number (IBAN) using the bank’s mobile application, internet banking, or visiting their bank branch.

“Once a customer has set her/his mobile phone number as the Raast ID, others can send money to her/him using her/his mobile phone number without the need to know the account number or any other details,” said the SBP.

Bank customers can still use Raast service for sending or receiving funds using their IBANs even if they do not have a Raast ID or prefer to use their IBAN.

The SBP has directed all banks to make Raast P2P fund transfer service available on at least three customer channels including mobile application, internet banking and branch counters.

The list of banks that have completed the necessary technological upgrades and other needed preparations and are offering Raast P2P services to their account holders as of today has been issued, said the SBP.

Twitter Feed

Live Traffic Feed

Sponsored Links

South Asia Investor Review

Investor Information Blog

Haq's Musings

Riaz Haq's Current Affairs Blog

Please Bookmark This Page!

Blog Posts

Pakistani Student Enrollment in US Universities Hits All Time High

Pakistani student enrollment in America's institutions of higher learning rose 16% last year, outpacing the record 12% growth in the number of international students hosted by the country. This puts Pakistan among eight sources in the top 20 countries with the largest increases in US enrollment. India saw the biggest increase at 35%, followed by Ghana 32%, Bangladesh and…

ContinuePosted by Riaz Haq on April 1, 2024 at 5:00pm

Agriculture, Caste, Religion and Happiness in South Asia

Pakistan's agriculture sector GDP grew at a rate of 5.2% in the October-December 2023 quarter, according to the government figures. This is a rare bright spot in the overall national economy that showed just 1% growth during the quarter. Strong performance of the farm sector gives the much needed boost for about …

ContinuePosted by Riaz Haq on March 29, 2024 at 8:00pm

© 2024 Created by Riaz Haq.

Powered by

![]()

You need to be a member of PakAlumni Worldwide: The Global Social Network to add comments!

Join PakAlumni Worldwide: The Global Social Network