PakAlumni Worldwide: The Global Social Network

The Global Social Network

Pakistan's Fiscal Year 2022 GDP Reaches $1.62 Trillion in Purchasing Power Parity (PPP) Terms

Economic Survey of Pakistan 2021-22 confirms that the nation's GDP grew nearly 6% in the current fiscal year, reaching $1.62 Trillion in terms of purchasing power parity (PPP). It first crossed the trillion dollar mark in 2017. In nominal US$ terms, the size of Pakistan's economy is now $383 billion. In terms of the impact of economic growth on average Pakistanis, the per capita average daily calorie intake jumped to 2,735 calories in FY 2021-22 from 2,457 calories in 2019-20. Pakistan experienced broad-based economic growth across all key sectors in FY 21-22; manufacturing posted 9.8% growth, services 6.2% and agriculture 4.4%. The 4.4% growth in agriculture is particularly welcome; it helps reduce rural poverty. The country's per capita income is $1,798 in nominal terms and $7,551 in PPP dollars. These figures do not yet show up in Google searches. Under former Prime Minister Imran Khan's leadership, Pakistan succeeded in achieving outstanding economic growth and nutritional improvements in spite of surging global food prices amid the Covid19 pandemic. Increasing energy consumption and soaring global energy prices have rapidly depleted Pakistan's forex reserves, forcing the country to seek yet another IMF bailout. History tells us that these bailouts have been forced whenever Pakistan's GDP growth has exceeded 5%. The best way for Pakistan to accelerate its growth beyond 5% in a sustainable manner is to boost its exports by investing in export-oriented industries, and by incentivizing higher savings and investments.

|

| Pakistan Economic Data. Source: IMF April 2022 |

The IMF (International Monetary Fund) has updated its website in April, 2022 with data reported for FY 2020-21. It's not unusual for the IMF data reporting to lag by a year or more. Pakistan's Economic Survey 2021-22 was published in June, 2022.

|

| Sector-wise Economic Growth. Source: Economic Survey of Pakistan 20... |

Pakistan experienced broad-based economic growth across all key sectors in FY 21-22; manufacturing posted 9.8% growth, services 6.2% and agriculture 4.4%. The 4.4% growth in agriculture is particularly welcome; it helps reduce rural poverty.

In terms of the impact of economic growth on average Pakistanis, the per capita average daily calorie intake jumped to 2,735 calories in FY 2021-22 from 2,457 calories in 2019-20. The biggest contributor to it is the per capita consumption of fresh fruits and vegetables which soared from 53.6 Kg to 68.3 Kg, less than half of the 144 Kg (400 grams/day) recommended by the World Health Organization. Healthy food helps cut disease burdens and reduces demand on the healthcare system. Under former Prime Minister Imran Khan's leadership, Pakistan succeeded in achieving these nutritional improvements in spite of surging global food prices amid the Covid19 pandemic.

|

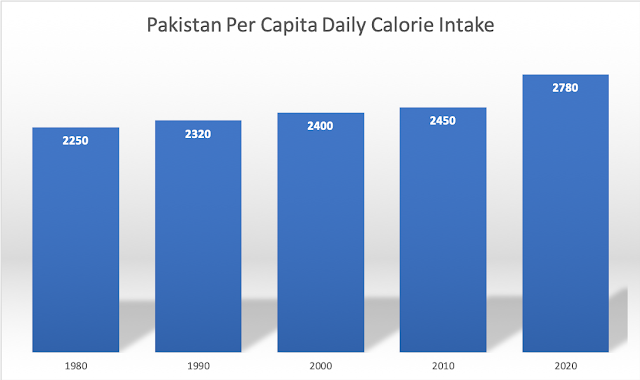

| Pakistan Per Capita Daily Calorie Consumption. Source: Economic Surveys of Pakistan |

The trend of higher per capita daily calorie consumption has continued since the 1950s. It has risen from about 2,078 in 1949-50 to 2,400 in 2001-02 and 2735 in 2021-22. The per capita per day protein intake in grams increased from 63 to 67 to about 75 during these years. Health experts recommend that women consume at least 1,200 calories a day, and men consume at least 1,500 calories a day, says Harvard Health Publishing. The global average has increased from 2360 kcal/person/day in the mid-1960s to 2900 kcal/person/day currently, according to the Food and Agricultural Organization (FAO). The USDA (United States Department of Agriculture) estimates that most women need 1,600 to 2,400 calories, while the majority of men need 2,000 to 3,000 calories each day to maintain a healthy weight. Global Hunger Index defines food deprivation, or undernourishment, as consumption of fewer than 1,800 calories per day.

|

| Share of Overweight or Obese Adults. Source: Our World in Data |

The share of overweight or obese adults in Pakistan's population is estimated by the World Health Organization at 28.4%. It is 20% in Bangladesh, 19.7% in India, 32.3% in China, 61.6% in Iran and 68% in the United States.

|

| Major Food Items Consumed in Pakistan. Source: Economic Survey of P... |

The latest edition of the Economic Survey of Pakistan estimates that per capita calories come from the annual per capita consumption of 164.7 Kg of cereals, 7.3 Kg of pulses (daal), 28.3 Kg of sugar, 168.8 liters of milk, 22.5 Kg of meat, 2.9 Kg of fish, 8.1 dozen eggs, 14.5 Kg of ghee (cooking oil) and 68.3 Kg of fruits and vegetables. Pakistan's economy grew 5.97% and agriculture outputs increased a record 4.4% in FY 2021-22, according to the Economic Survey. The 4.4% growth in agriculture has boosted consumption and supported Pakistan's rural economy.

The minimum recommended food basket in Pakistan is made up of basic food items (cereals, pulses, fruits, vegetables, meat, milk, edible oils and sugar) to provide 2150 kcal and 60gram protein/day per capita.

The state of Pakistan's social sector is not as dire as the headlines suggest. There are good reasons for optimism. Key indicators show that nutrition and health in Pakistan are improving but such improvements need to be accelerated.

South Asia Investor Review

Pakistan's Expected Demographic Dividend

Pakistan's Social Sector

World Bank: Pakistan Reduced Poverty, Grew Economy During Covid19 P...

Surging Global Food Prices Amid Covid Pandemic

Pakistan's Balance of Payments Crisis

Panama Leaks in Pakistan

Olive Revolution in Pakistan"

Nay Pakistan Sehat Card: A Giant Step Toward Universal Healthcare

Prime Minister Imran Khan's Effectiveness as Crisis Leader

India in Crisis: Unemployment and Hunger Persists After Waves of Covid

Riaz Haq's Youtube Channel

Views: 1226

-

Comment by Riaz Haq on April 30, 2023 at 11:02am

-

Flour crisis deepens in Pakistan | World Grain

https://www.world-grain.com/articles/18326-flour-crisis-deepens-in-...

ISLAMABAD, PAKISTAN — Despite slight increases expected for wheat production and imports in Pakistan, consumption is forecast to outstrip supply in marketing year 2023-24 in the country with the world’s fifth largest population, according to a Global Agricultural Information Network report from the Foreign Agricultural Service of the US Department of Agriculture (USDA).

Although a slight reduction in planted area is anticipated, wheat production in Pakistan is projected to increase 2% to 27 million tonnes, with wheat yield expected to rise due to favorable weather conditions and better availability of irrigation water. However, wheat consumption is forecast to increase 3% in 2023-24, the USDA said, in one of the fastest growing countries in the world with a population of 233 million. The shortage of wheat, which accounts for 72% of Pakistan’s daily caloric intake, has caused a flour-availability and affordability crisis in Pakistan.

“High inflation has made it difficult for consumers to afford milk and meat, reversing the trend of more protein and less carbohydrates in the diet,” the USDA said. “As a result, consumption of wheat flour-based products is rebounding.”

But the supply is not rebounding at the same rate, in part due to the weather, the Russia-Ukraine war and other factors, causing many of the country’s citizens to wait in long lines in hopes of getting a bag of government-subsidized flour. Dozens of people have been trampled to death or injured in recent weeks when crowds have rushed forward to try to get the flour.

According to a recent World Food Programme report, the prices for staple cereals, pulses, and non-cereal food commodities continue to increase in Pakistan. It noted that the price of wheat flour has increased by 74% year-on-year.

“The price of wheat and wheat flour has continued to increase in the country due to various factors, including the tight supply of private wheat, hoarding and profiteering,” the WFP report said.

-

-

The wheat production (in Pakistan) this year topped 27.5 million metric tons, the highest in the last 10 years, despite the challenges posed by heavy rains and floods last year, the Prime Minister’s Office said in a statement on Sunday.

https://tribune.com.pk/story/2414418/pm-hails-bumper-wheat-crop

Chairing a review meeting on the wheat situation, Prime Minister Shehbaz Sharif directed the relevant federal government institutions as well as the provinces to increase their procurement quotas in the wake of a bumper crop.

According to the Prime Minister’s Office, the meeting received a briefing on the wheat production, current reserves, carry-forward reserves, procurement targets, and progress of federal and provincial departments.

Shehbaz applauded the record wheat production, saying that this achievement made possible by the grace of Allah, quality seeds, uninterrupted supply of fertiliser, and the timely decisions of the government and its Farmers Package.

“The bumper crop of wheat is a testament to the government’s timely decisions and excellent governance,” he said. “Looking forward, the government is preparing a strategy to increase wheat production even further next year,” he added.

“With the government’s continued efforts and the dedication of farmers, Pakistan aims to maintain its position as a leading wheat producer,” he said, congratulating the farmers for their hard work and dedication to achieve the milestone despite financial difficulties.

He noted that Pakistan became a wheat importing country due to the mismanagement of the previous Pakistan Tehreek-e-Insaf (PTI) government. The PTI government, he added, made farmers to stand in long queues for fertilisers.

He urged the federal and provincial institutions to increase procurement targets to enable uninterrupted supply of wheat throughout the year. He also instructed that the resources required to obtain the specified quantity of wheat should be provided through banks.

He congratulated Food Security Minister Tariq Bashir Cheema and the officials concerned, and directed all institutions to increase their targets. The meeting was also attended by the caretaker Punjab minister for industries, and other senior officials.

-

-

A brewing up controversy over GDP growth figures. The revised estimates suggests that the last fiscal year growth went up to around 6.5 percent against provisional figure of 5.97 percent @ NAC meeting postponed

https://www.thenews.com.pk/print/1071476-nac-meeting-postponed

At the last moment, a National Accounts Committee (NAC) meeting scheduled for Thursday (today) has been postponed apparently on the pretext that some census data will be incorporated into it for calculating the provisional GDP growth figure and per capita income.

However, top sources confided to The News on Wednesday that efforts were still under way to turn the possible negative growth figures into positive despite witnessing a steep fall in the figure of Large-Scale Manufacturing (LSM) in March 2023 whereby it contacted by 25 per cent. In July-March period of the current fiscal, the LSM dropped by 8.1 per cent. There are some more worrying developments as the initial estimates suggest that the finalized figure of GDP growth for the last financial year went up from the provisional figure of 5.97 per cent to finalized figure of 6.5 per cent for 2021-22 so the revised GDP growth figure would also result in showing more declining figure of provisional growth in the outgoing financial year 2022-23. Where there was a higher base, it would negatively affect the provisional growth prospects for the outgoing financial year, said the sources.

“The latest estimates suggest that the provisional GDP growth is negative so far in the range of -0.8 per cent to -1 per cent for the current fiscal year 2022-23,” said the sources and added that it could not be yet ascertained how the provisional GDP growth figures would be turned into positive one. Now the NAC may be rescheduled for Friday (tomorrow), but the Pakistan Bureau of Statistics (PBS) has not yet issued an official notification on the NAC meeting. However, one top official told The News that on the request of the PBS, the NAC meeting was rescheduled for Friday because the latest census data might be incorporated for calculating the provisional GDP growth figures and the per capita income in both rupee and dollar terms.

Pakistan envisaged GDP growth target of 5 per cent for the current financial year 2022-23 on the eve of the budget with the help of agriculture growth target of 3.9 per cent, manufacturing 7.1 per cent and services sector 5.1 per cent. The IMF and the World Bank had projected a downward revision of GDP growth in the range of 0.5 per cent for the current fiscal year. The Ministry of Finance had projected growth rate of 0.8 per cent in its revised estimates for the current financial year. The agriculture sector growth may also remain negative and it will solely depend upon the factor of wheat production. Among the services sector, the credit to private sector witnessed new low as the private sector credit from banks stood at just Rs 72 billion so far in the current fiscal year against Rs 800 billion in the same period of the last financial year.

The Wholesale and Retail trade might also witness declining trends, keeping in view imports compression. On eve of the budget for 2022-23, the government had envisaged GDP growth rate at 5 per cent and inflation at 11.5 per cent. Now the average CPI based inflation is expected to hover around 29-30 per cent on average for the current fiscal year.

-

-

4 reasons India won’t overtake China as the world’s agricultural commodity hub any time soon | South China Morning Post

https://www.scmp.com/comment/opinion/article/3221894/four-reasons-i...

At the lowest income levels, food is consumed in its most basic form as whole grain or in simple porridges. As incomes rise, that grain is increasingly consumed indirectly – it could be baked into bread or fed to animals for meat production. Each subsequent stage requires further processing, as well as additional ingredients such as oil and sugar to complete formulations.

exponential increases in higher-value food consumption take hold as incomes grow from US$1,000 and US$10,000 before plateauing above US$20,000. A large, young and rapidly growing population base with incomes rising from modest to median levels makes an ideal environment for agricultural commodity demand growth.

------------------

India recently overtook China as the world’s most populous country, according to UN projections. Around one in three people on the planet now lives within the borders of these two nations.

The media frenzy surrounding the revelation centred on the economic implications of India’s new status, much to the chagrin of the Chinese authorities. The question now arises as to what this means for the global agricultural market.

Since the dawn of the Malthusian spectre, population growth has been associated with a reduction in living standards. As the theory goes, populations grow faster than the resources required to feed them.

China has been able to defy that thesis in the past two decades, combining a growing population with consistent income growth. It has become the largest buyer of key agricultural commodities to ensure its inhabitants enjoy a diversified diet.

China is now a top importer of the most widely traded crops globally: soybeans, vegetable oil, corn and sugar. With that, Beijing wields enormous influence in this space. Chinese demand has caused explosive growth in South American soybean production, leading Brazil to pass the United States as the world’s leading producer of soybeans and prompting Argentina to become the top exporter of soybean meal.

-

-

Sugar production/consumption in Pakistan

Due to slight increases in area and sugarcane yields, sugar production in 2022/23 is forecast to reach 7.2 million metric tons (MMT), a marginal increase over the good 2021/22 crop. Sugar consumption for 2022/23 is forecast at 6.1 MMT (approx 26 Kg per person) , which would be a 3.3 percent increase, reflecting population growth and demand from the expanding food processing sector. The production estimate for 2021/22 is increased reflecting the excellent crop last year. As a result, ending stocks are higher, leading to a larger exportable surplus entering 2022/23. Due to the large stocks, and competitive prices, sugar exports are forecast to reach one million tons in 2022/23

https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFil...

----------

Sugar production/consumption in India

Assuming normal rainfall and favorable weather conditions, India’s centrifugal sugar production in marketing year (MY) 2021/22 (October-September) is forecast to grow three percent to 34.7 million metric tons (MMT) (equivalent to 31.8 MMT of crystal white sugar) on a sugarcane production forecast of 389 MMT. Uttar Pradesh will continue to be the largest sugar producing state, followed by Maharashtra and Karnataka. India will retain its existing export policy that will enable subsidized exports at six MMT. Consumption is forecast to rise two percent to 28.5 MMT (approx 20 Kg per person), as the economy recovers from the pandemic. Closing stocks are estimated at 16.5 MMT and expected to further decline as India diverts more sugar toward ethanol production to meet its domestic blending mandate.

https://www.fas.usda.gov/data/india-sugar-annual-5#:~:text=Sugar%20....

-

-

As of March 2023, Pakistani authorities still ban genetically engineered (GE) oilseed imports. While they have made some progress in developing a system to allow for GE oilseed imports, uncertainty regarding when that system will be operative clouds the outlook for oilseed imports. Similar uncertainty surrounds domestic meal and oil production forecasts. With expectations for better cottonseed production, total oilseed production in 2023/24 is projected to increase to 2.95 million tons, a 24 percent above than 2022/23. In line with population growth, edible oil demand is forecast to grow about 5 percent, and palm oil imports are forecast to grow accordingly, reaching 3.6 million tons (15 Kg per person) in 2023/24.

https://www.fas.usda.gov/data/pakistan-oilseeds-and-products-annual-7

----------------

India’s oilseeds production in marketing year (MY) 2023/2024 (October-September) is forecast to remain flat at 41.5 million metric tons (MMT), mostly unchanged from MY 2022/2023. Unseasonably heavy spring precipitation and a predicted El Niño weather pattern in the wake of severe April-June heatwaves will expose summer oilseed crops to greater incidences of plant stresses and thus impact yields. Oil meal production will remain steady at 20 MMT while exports will fall to 1.9 MMT, following an exceptional increase in exports in the current MY as southeast Asian demand has favored competitively priced Indian oil meals against other origins. India will remain among the largest consumers of edible oils and is forecast to import 14.5 MMT (10 Kg per person) of various oil commodities in the outyear. Global decline in oilseed prices and relatively low import duties have stabilized domestic edible oil prices, leading to record ending stocks in the current year.

https://www.fas.usda.gov/data/india-oilseeds-and-products-annual-7

Comment

- ‹ Previous

- 1

- …

- 5

- 6

- 7

- Next ›

Twitter Feed

Live Traffic Feed

Sponsored Links

South Asia Investor Review

Investor Information Blog

Haq's Musings

Riaz Haq's Current Affairs Blog

Please Bookmark This Page!

Blog Posts

Pakistani Prosthetics Startup Aiding Gaza's Child Amputees

While the Israeli weapons supplied by the "civilized" West are destroying the lives and limbs of thousands of Gaza's innocent children, a Pakistani startup is trying to provide them with free custom-made prostheses, according to media reports. The Karachi-based startup Bioniks was founded in 2016 and has sold prosthetics that use AI and 3D scanning for custom designs. …

ContinuePosted by Riaz Haq on July 8, 2025 at 9:30pm

Indian Military Begins to Accept Its Losses in "Operation Sindoor" Against Pakistan

The Indian military leadership is finally beginning to slowly accept its losses in its unprovoked attack on Pakistan that it called "Operation Sindoor". It began with the May 31 Bloomberg interview of the Indian Chief of Defense Staff General Anil Chauhan in Singapore where he admitted losing Indian fighter aircraft to Pakistan in an aerial battle on May 7, 2025. General Chauhan further revealed that the Indian Air Force was grounded for two days after this loss. …

ContinuePosted by Riaz Haq on July 5, 2025 at 10:30am — 6 Comments

© 2025 Created by Riaz Haq.

Powered by

![]()

You need to be a member of PakAlumni Worldwide: The Global Social Network to add comments!

Join PakAlumni Worldwide: The Global Social Network