PakAlumni Worldwide: The Global Social Network

The Global Social Network

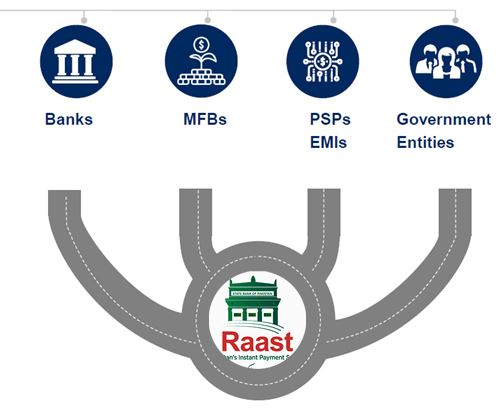

Raast Aims to Create Pakistan's Unified Digital Payments Infrastructure

Pakistan's central bankers have taken the plunge into the world of digital payments with their own offering: Raast. It aims to create an instant low-cost payment system that can seamlessly and securely connect government entities, a variety of banks, including microfinance banks (MFBs), electronic money institutions (EMIs) and State Bank authorized payment service providers (PSPs) like 1Link and NIFT which may choose to take advantage of it. Currency and coins in circulation account for about 43% of Pakistan's total money supply. The introduction of Raast is part of the government's effort to modernize and document the nation's cash-based informal economy. Undocumented economy poses a serious threat to the country because it creates opportunities for criminal activities and tax evasion. Digital financial services will also promote e-commerce in Pakistan.

|

| Raast Digital Payment System. Source: State Bank of Pakistan |

Raast Digital Payments:

Raast is a system of digital payment infrastructure. It is essentially a pipe that is intended to connect government and financial institutions with consumers and merchants with each other to process payments instantly at very low cost.

Raast will be boosted by Pakistan government's decision to use it to pay salaries, pensions and pay welfare recipients under Benazir Income Support and Ehsaas Emergency Cash programs.

State Bank of Pakistan intends to demonstrate Raast's usefulness by first processing government payments to individuals, including government employees and Ehsaas welfare beneficiaries, before expanding it for business applications. SBP’s plan is to start person-to-person (P2P) payments using just the phone numbers in Q3/2021 and then bring merchants on board with QR codes by Q1/2022.

Pakistan's Sadia Zahidi Leads WEF Gender Equity Effort

Brothers From Rural Pakistan Teaching AI to American High Schoolers

Pakistan's Computer Services Exports Jump 26% Amid Coronavirus Lock...

Pakistan Gig Economy Among World's Fastest Growing

Digital BRI and 5G in Pakistan

Pakistan's Demographic Dividend

Pakistan EdTech and FinTech Startups

State Bank Targets Fully Digital Economy in Pakistan

Campaign of Fear Against CPEC

Fintech Revolution in Pakistan

E-Commerce in Pakistan

The Other 99% of the Pakistan Story

FMCG Boom in Pakistan

Belt Road Forum 2019

Fiber Network Growth in Pakistan

Riaz Haq's Youtube Channel

Views: 1499

-

Comment by Riaz Haq on January 23, 2021 at 5:18pm

-

China prepares to launch the world’s first official e-currency

Party leaders believe the country’s big tech platforms have too much powerhttps://www.economist.com/the-world-ahead/2020/11/17/china-prepares...

THERE IS A good chance that the digital yuan will enter circulation in 2021. It is a debut that will initially make little difference, but could, over time, change the way central banks conduct monetary policy.

The People’s Bank of China has filed more than 100 patent applications for a digital currency and has overseen a range of trials, putting the e-yuan into use in a few cities and on several apps. So far the experiments have gone smoothly, and soon people will have the option of downloading a government-issued digital wallet. Unlike commercial ones such as WeChat Pay and Alipay, the official version will be equivalent to an account at the central bank with the same solidity as hard cash.

For the millions who already use a smartphone instead of a debit card, it will feel like just another payment app. Yet some talk of digital currency as a revolutionary product that could spell trouble for banks as people withdraw money from savings accounts and put it directly into their ultra-safe official e-wallets. What is more, if digital currency were ever to fully replace cash, central banks would, in theory, gain three new powers: to lower interest rates below zero with little difficulty; to issue cash directly to those most in need; and to see more precisely who has money and how it is spent.

In China the central bank is not trying to reinvent monetary policy—at least not yet. Its motivations derive from more immediate challenges. Given the rise of mobile payments, it worries that the big tech platforms have too much power. The digital yuan will offer an alternative. It will also give China a conduit for moving money across its borders without having to rely on swift, a global payments system that comes under American influence. But China’s first objective is much more basic still: to check whether the technology behind the digital yuan works and whether people actually want to use it. Money has been around for some 3,000 years. This update will take time.

-

-

Karandaaz Chief Digital Officer Rehan Akhtar told The Express Tribune that Raast is not a bank or a mobile wallet, rather it is a backend payment system similar to 1link, which intends to take all banks of the country on board to offer the public an optimal digital payment experience.

https://tribune.com.pk/story/2281336/raast-optimal-digital-payment-...

“Banks and mobile wallets motivate people to open accounts so that respective service providers can facilitate their customers in conducting transactions through digital applications or internet portals,” he said.

“On the other hand, no mobile application will be launched for Raast and instead, banking applications and portals will offer payment through the Raast mechanism.”

He added that all banks will be taken on board for offering payments through the Raast mode.

Akhtar pointed out that one banking institution alone cannot develop financial infrastructure for all its customers, therefore, banks collaborated with companies offering payment solutions to enhance their services and cover all their customers. Raast is one such system, he said.

He talked about the concept of intra-operability through which payment solutions aid bank customers in withdrawing money from even those ATMs that do not belong to their respective banking institution. However, it comes with a fee.

“Intra-operability exists in the telecom sector as well, which lets consumers make calls from local networks while they are abroad and that too comes with a fee,” he said. “If intra-operability is compromised, it is the customer who suffers.”

He emphasised that Raast is aimed at resolving the issues present in account-to-account intra-operability among banks.

The Inter Bank Fund Transfer system is underutilised in Pakistan because of high fee and complicated procedures.

Detailing about the arduous procedures, he said that to transfer funds, a customer needs the name of banking institution and 10-14 digit account number of the other party. “This information needs to be verified and finally a high fee is charged for the transfer, which discourages micro transactions through this mode altogether.”

According to him, intra-operability should be a seamless experience and that is exactly what Raast plans to achieve.

He added that a directory is planned to be created in the Raast system, which will simplify payment addresses for swift fund transfer.

The directory will allot an alias to the accountholder, which will make it easier to trace the person and transfer money between two accounts in different banking institutions.

“There will either be a low fee or no fee at all on the intra-bank fund transfer through Raast, which will act as a massive incentive for consumers,” he said.

The official said that the system’s simplicity coupled with the directory is what has made it unique.

He elaborated that there will be three use cases for the payment system.

In the first case, the government can use Raast to pay stock dividends, government salaries and payments under the Ehsaas programme.

Moving on to the second case, he said person-to-person use of the system will allow the transfer of amounts between two individual accounts. However, this mechanism is yet to be activated. Third case is the use of Raast by a merchant.

He added that if a merchant receives digital payment, then banks take two to five days to settle the amount, which can impact the cash flow for businessmen, particularly those who have to buy merchandise on a daily basis.

Raast will soon launch a merchant scheme similar to Visa with excellent efficiency, he said. Raast has the capacity to operate multiple settlement processes per day and merchants will receive their amounts on the same day.

Finally, he explained, there will be request-to-pay option that will enable merchants to demand payment for products through the service so that they receive the exact amount digitally, which eliminates chances of fraud.

-

-

In the move toward digital payments in cash-centric economies, building trust in bank accounts and payments done in bits and bytes is critical.

https://www.pymnts.com/digital-payments/2021/bridging-cash-digital-...

In Pakistan, for firms seeking to spur that adoption and to foster financial inclusion, it’s important to have a “cash in, cash out” mindset, as Erwan Gelebart, CEO of digital wallet, mobile payments and digital banking provider JazzCash, told Karen Webster in an interview.

At the time of this writing, JazzCash (owned by VEON, a global telecommunications and digital services firm) has 12 million active users in Pakistan, where 80 percent of the adult population is unbanked. According to the World Bank, that represents a total of 100 million individuals. This, of course, represents a significant opportunity for firms seeking to broaden financial inclusion.

In terms of mechanics, the JazzCash Mobile Account is a bank account that is linked to users’ mobile numbers, allowing users to send and receive funds, pay bills, take out and pay loans, and conduct other everyday financial activities.

The business model is akin to mobile banking services seen in other parts of the world, such as M-PESA, which in a nutshell leverage mobile devices to facilitate the flow of money, rather than relying on banks or wallets that are in turn issued by third parties.

Apps — And Agents, Too

Users can register for and open accounts by downloading the JazzCash mobile app from Google Play or Apple’s App Store. But in a wrinkle — and with a nod to the “cash in, cash out” feature — the users also can visit one of over 60,000 JazzCash agents located in Pakistan, who can help users set up and use their JazzCash accounts (and transact in cash to buy goods).

Call it a way of bridging the divide between digital transactions and those rendered in bills and coins. Individuals and merchants just starting on their journey of getting comfortable with digital payments are happy to have agents that are “a few meters from where they are. That footprint is important,” Gelebart noted.

Cash In, Cash Out

At a high level, said Gelebart, “the customers are digitizing the cash they have with them” as they interact with a network of more than 40,000 merchants across the country and overcome obstacles to accessing the traditional banking system.

One key distinction is that the account itself is free of charge – and at present, there is even a sign-up bonus for new users equivalent to 30 U.S. cents, which helps spur adoption (especially on the merchant side). And fees are not incurred until users actually take advantage of the services on offer and transact.

Drilling down into the use cases, Gelebart noted that face-to-face transactions are not a pain point in daily commerce, as people are very much used to, and comfortable with, using cash. But remittance does have friction, as cross-border transactions involve costs and risks.

Gelebart pointed to a May 2020 announcement with Mastercard, where JazzCash users can apply for physical debit cards, while merchants can accept digital payments from their customers and move toward cashless operations.

With a nod toward the merchants, he said the company is running a pilot program that leverages the data collected through transactions and other business activities to generate risk scores and lend money to those corporate clients.

“We can create a profile, a risk profile, and the merchants can get an instant loan. They can go to their interface, the JazzCash business account,” he told Webster. “And in a few seconds, if they’re eligible, they will get the money directly in their account. It’s about adding more value to the JazzCash business accounts. And as a result, receiving and collecting payments digitally will start making sense for them” – especially as they can log their sales functions directly into the business account (which, in turn, provides richer data to JazzCash as it designs new commercial offerings).

-

-

Pakistan: Digital payments boom under Covid-19 lockdown

Mobile wallet penetration is currently low with the total number of accounts standing at 46mn (34% of the adult population) and active accounts at 25mn (18% of ...

https://tellimer.com/article/pakistan-digital-payments-boom-under-c...

Easypaisa, a leading digital wallet in Pakistan, reported a significant increase in activity during the lockdown

This is an indication, and reinforces our view, that Covid-19 could drive a shift to digital payments in Pakistan

Pakistan represents an ideal environment for digital banking to thrive

----------------

The report draws insights from a regional survey, which polled more than 5,000 consumers in the UAE, Saudi Arabia, Egypt, Jordan, Qatar, Kuwait, Bahrain and Pakistan.

https://www.computerweekly.com/news/252493293/Covid-19-sparks-boom-...

Across those countries, 47% of consumers said they expected to shop online more frequently over the next year. Only 15% expected their online shopping frequency to decline, while the remaining 38% expected it to remain the same.

The likely surge in e-commerce and digital payments in 2021 is consistent across the countries surveyed, with 49% of Gulf Cooperation Council (GCC) consumers saying they will shop online more frequently, and 48% in Jordan, 47% in Egypt and 39% in Pakistan saying the same.

Mo Ali Yusuf, regional manager at Checkout.com, said Covid-19 was driving a “significant share” of e-commerce and digital payment transactions in the Middle East, with 40% of online shoppers saying they are buying and paying online because of the pandemic.

“We’ve witnessed this steady shift to digital payments over the past six years, but the pandemic has really served as a catalyst – condensing five years of growth into a matter of months,” Yusuf told Computer Weekly.

“While there has been a sudden surge in e-commerce and digital payments this year due to the impact of Covid-19, what we are seeing today is more than a temporary change in consumer behaviour.”

Yusuf said that despite a big uptake in digital payments across the Middle East in the last few years, cash on delivery still occupies a significant proportion of share of wallet for consumers.

“This presents a market with huge potential for continued growth over the next decade,” he pointed out.

Preference for digital payments over cash on delivery or bank transfers rises significantly as consumers shop online more frequently, according to the report. Among those who shop online at least once a month, 62% usually pay by card or digital wallet, compared with 44% among the less frequent online shoppers.

“Robust digital payment options have become an integral part of what consumers expect from merchants, especially as e-commerce is more widely embraced in the region,” said Yusuf.

According to Khalid Dannish, CEO of Bahrain Fintech Bay, the island’s fintech accelerator hub, the region is seeing a flood of new digital payments activity in the wake of Covid-19.

“The infrastructure and accessibility is now there for merchants and consumers,” he said. “The pandemic has changed consumer behaviour in a lasting way.

“Given the young nature of regional demographics, the preference is to move towards digital payment strategies not just for convenience but also for user experience. We are seeing digital payments being used for everything from meals to clothing to groceries and utilities.”

-

-

Citi has named Shahmir Khaliq as its new head of Treasury and Trade Solutions (TTS), according to an internal memo from Paco Ybarra, global head of Citi’s Institutional Clients Group (ICG), which noted that the appointment is effective immediately.

https://www.pymnts.com/personnel/2021/citi-names-khaliq-as-new-trea...

During his career at Citi, Khaliq has served in management positions in banking, markets and securities services, country management (CCO) and treasury services. Prior to his appointment as global head of TTS, Khaliq served as head of operations and technology for TTS. Before taking that role, Khaliq had served as global head of Direct Custody & Clearing inside of Markets and Securities Services since 2017.

Khaliq joined Citibank in 1991 in Pakistan as a management associate in the institutional bank before leaving in 1993 for his post-graduate education. He rejoined Citi Pakistan (Banking) in 1995.

Khaliq holds degrees in finance and economics from the London Business School and London School of Economics. He also has a master’s of business administration from the University of Karachi.

“[Khaliq’s] experience gives him a unique ability to understand our clients’ needs and to drive investment in our infrastructure and our network to ensure that we can continue to help them sustain their operations, manage their supply and distribution chains and optimize their working capital and liquidity. He will help improve our core product capabilities and rethink how we interact with clients from a coverage, sales and service perspective to deliver a continuously improving client experience,” Ybarra said in the memo.

TTS, which had been led by Naveed Sultan, offers cash management and trade finance services to multinational firms, public sector organizations and financial institutions throughout the world.

Sultan will head up the firm’s efforts to advise governments and other clients on digitization in a new position as ICG chairman, according to an October internal memo. He will be in charge of developing a new "digital policy, strategy and advisory practice" that will consult with governments aiming to digitize their economies and financial systems, among other tasks.

-

-

Naveed Sultan is Global Head of Treasury and Trade Solutions in Citi’s Institutional Clients Group. With over 25 years of institutional banking experience, Mr Sultan has been at Citi for over 20 years in a range of increasingly senior roles, and currently, is responsible for the business management of Treasury and Trade Solutions globally. This

multi-billion business is one of the largest global businesses encompassing multiple integrated solutions within Citi’s Institutional Clients Group including: Trade and Supply Chain, Export Agency Finance, Liquidity and Investment Management, Wholesale Cards Services, Information Services, Receivables, consulting and digital services serving public sector clients, corporates and financial institutions, a client base that includes 94% of the top 500 global companies, 700 public sector clients and 600 banks, asset managers and insurance companies in over 120 countries, Prior to his appointment to his current role in June 2011, Mr Sultan was the Transaction Services Region Head for Europe, Middle East and Africa (EMEA), the largest region for this business line with a presence in over 50 markets and a multi-billion dollar revenue base. Mr Sultan has served as a director on the board of LCH Clearnet, Citibank A.S (Turkey) and Citibank Europe Plc. He is also a member of the Operating and Management Committees of the Institutional Clients Group. He is a member of Citi’s Innovation Council and chairs the Global Innovation Council for Treasury and Trade Solutions. He is also a member of the Smart London Board; advisory board to Mayor of London. He joined Citi with Saudi American Bank (SAMBA), an affiliate of Citibank, in 1993 where he held several senior positions including Global Transaction Banking Group Head and Senior Country Operations Officer. In 1999, he became the business head for Citi's Transaction Bank for Western Europe, based in London. Before joining Saudi American Bank, Naveed was the Country Corporate Banking Head for Standard Chartered Bank in Pakistan. Mr Sultan has wide-ranging experience covering Corporate Banking, Corporate Finance, Transaction Banking, Operations & Technology and is a regular speaker and author on such topics. He has also taught Business to Masters graduates at the University of Punjab in Pakistan. He is also engaged with Imperial College and Oxford University in an advisory and lecturing capacity. Mr Sultan holds an M.S. in Management from M.I.T’s Sloan School of Management as well as an M.B.A. from the Institute of Business Administration, Lahore.

https://www.crunchbase.com/person/naveed-sultan

----------

Citi's ICG appoints insider Naveed Sultan as chairman

https://www.reuters.com/article/us-citigroup-moves/citis-icg-appoin...

Citigroup’s Institutional Clients Group on Thursday named insider Naveed Sultan as chairman, according to an internal memo seen by Reuters.

Sultan, who has been serving as the global head of Citi’s Treasury and Trade Solutions (TTS) since 2011, would build a new “Digital Policy, Strategy and Advisory practice” across all client segments, Citi ICG Chief Executive Officer Paco Ybarra said in the memo.

-

-

In Pakistan, and elsewhere, the stars are aligning for greater use of digital banking and payments to improve financial inclusion. To that end, Amir Wain, CEO of i2c Inc., told PYMNTS CEO Karen Webster in an interview that the pandemic and the rise of mobile infrastructure have set the stage to bring people living in developing and emerging economies into the digital realm.

https://www.pymnts.com/news/payment-methods/2021/super-apps-rising-...

In commerce and in the great pivot away from cash, challenges remain — tied to acceptance. As eCommerce has become more firmly entrenched in countries such as Pakistan, buying and selling goods by digital means (moving away from the cash-on-delivery model) has generated at least a “reasonable acceptance level,” according to Wain, that gets some critical mass through a few large anchor eCommerce merchants in each market.

“You have these ‘local Amazons’ that are cropping up,” he told Webster, “and if you integrate with them, then you have merchants in meaningful numbers driving digital currency activity. Once you have some activity going, you have to think about, how to continue to expand the acceptance network.’ ”

Mobile plays a big part in increasing acceptance, said Wain, as it provides an alternative to point of sale (POS) terminals, land lines that’s easy to deploy and maintain.

QR codes and even peer-t0-peer (P2P) options are gaining favor, especially for smaller retailers.

Regulators are also getting on board with letting NFIs offer financial products in emerging economies, broadening the financial services ecosystem, said Wain. The greenfield opportunities are also attracting significant numbers of entrepreneurs and capital to countries like Pakistan.

All of these factors create a “perfect combination for digital payments to take off in these markets,” he said.

Issuance Matters, Too

Issuing plays a critical role too — as Webster stated, users need secure credentials in place to transact.

“This is where you will find weaknesses and hence will see a lot of improvement over the next few years,” predicted Wain, “People who do not have experience with the issuing business underestimate its complexities. To them, transferring $10 from one account to another appears fairly simple. But there is a lot more to having a secure and stable issuer processing system. System integrity, handling of leading-edge cases and compliance are some of the areas often overlooked. And let’s not forget there are plenty of fraudsters who are looking for system weaknesses that they can exploit.”

Bad actors may be lured by the relatively immature infrastructure. In other cases, apps are too slow, or user interfaces are clunky. In the end, though, evolution is inexorable — and we are evolving toward super apps. With a nod toward Pakistan as a specific market, Wain noted that there is no dominant super app yet — but the conditions now exist for such an offering to take root.

In terms of numbers, he said, the population of 220 million represents a significant market and there are 100 million mobile users (with approximately 70 million smartphones in the market), and counting.

Among the many features tied to the super app, due to launch in the first quarter, P2P proves to be especially useful for people sending money to rural areas — and which will help bring them toward using more services as time goes on. That functionality helps fill a vacuum left by larger, traditional financial institutions (FIs), said Wain, which tend to be slow in responding to consumers’ needs, and where it’s proven difficult to serve individuals’ “small ticket needs” through expensive branches.

-

-

It takes a certain kind of person to move in next door to their boss. Today the biggest question in Swiss banking is just what kind of person Iqbal Khan is.

https://www.ft.com/content/ba0d47be-e0fc-11e9-b112-9624ec9edc59

Three months ago, Mr Khan, whose rapid ascent at Credit Suisse had marked him out to many as the heir apparent to chief executive Tidjane Thiam, quit his senior position at the bank. This week, details emerged of a bitter row between Mr Khan, 43, and Mr Thiam, 57, triggered by a confrontation in central Zurich between the private banking prodigy and detectives Credit Suisse had hired to monitor him after he resigned.

It was a lurid end to a spectacular dispute between two of the most powerful men in finance — one from which Mr Khan may yet emerge triumphant. On Tuesday, he is due to take up a senior position at UBS, which would make him a likely successor to Sergio Ermotti as the bank’s chief executive. Mr Ermotti is known to admire Mr Khan’s relentless ambition, prizing it over the qualities of other more rounded contemporaries. Meanwhile, UBS’s chairman, Axel Weber, has taken a dimmer view of the spectacle, according to a person who knows him.

Bruising rows between big egos are not new in the world of finance. But the suburban dimension to Mr Khan’s collision with his boss has given it a distinctive flavour. After he boldly moved into the house next door to Mr Thiam’s two years ago, the pair channelled a simmering generational workplace conflict into bickering over house improvements and blocked views. The dispute climaxed in a row at a neighbourhood cocktail party in January.

“To me, moving in next door like that, there are two signals you might be wanting to send,” says one Credit Suisse executive. “Either: ‘We get along so well I’d like to spend more time near you,’ or else: ‘I’m coming for you.’”

Yet the image of an overweening princeling is only part of the picture. Many of those who have worked with Mr Khan recognise different sides to his personality.

-

-

A top adviser to UBS private bank co-head Iqbal Khan won a major promotion as part of a shake-up of the Swiss bank's strategy and corporate development team, finews.asia can reveal.

https://www.finews.asia/finance/33548-ubs-michael-bonacker-christia...

Zurich-based UBS is tasking Christian Zeinler with group strategy, from February 1, according to a memorandum seen by finews.asia. Zeinler is head of strategy and business development at UBS' flagship $2.6 trillion wealth management arm – a job he will retain – as well as chief of staff to Iqbal Khan, who co-runs the unit.

The change was set into motion by the departure of Michael Bonacker, who had held the top strategy job since 2017, and will leave by mid-year. Bonacker, an ex-McKinsey partner who held top roles at Deutsche Bank, Lehman Brothers, and Commerzbank before joining UBS, was instrumental in the Swiss bank's strategy reviews since 2017.

-

-

Pakistan govt planning to launch country’s first-ever IPG (International Payment Gateway)

https://www.brecorder.com/news/40061735/govt-planning-to-launch-cou...

The government is planning to launch Pakistan’s first-ever “International Payment Gateway (IPG)” to advance the nation’s digital infrastructure in order to provide ease of doing business to the digital users globally.

The Ministry of Information Technology and Telecommunication and the National IT Board (NITB) under the auspices of the government of Pakistan will launch Pakistan’s first-ever IPG.

“We are aiming for User’s Digital payments with ease, convenience, and enhanced safety. In this regard, we are adopting user sensitive inclusive approach and request our users to provide a detailed feedback regarding the features for enhanced usability of IPG,” the ministry added.

As a freelancer, an e-commerce retailer and as a small trader one has to define his or her needs for international payments.

The ministry has also asked the concerned people to share difficulties they are facing in receiving international payments. Further, the ministry has sought details of security-related aspects in receiving international payments, concerns related to fraud-related aspects in international and cross-border payments, and what they would like to have the government of Pakistan provide to meet their special and particular needs international and cross-border payments.

Twitter Feed

Live Traffic Feed

Sponsored Links

South Asia Investor Review

Investor Information Blog

Haq's Musings

Riaz Haq's Current Affairs Blog

Please Bookmark This Page!

Blog Posts

Pakistan Joins China in World AI Cooperation Organization (WAICO)

On July 16 in Shanghai, 29 countries, including China, Pakistan and Russia, signed the founding agreement of WAICO, World AI Cooperation Organization. Every BRICS founding member is in, except India. This agreement follows the launch of the US-led Pax Silica, a 24-member coalition, including India, which is designed to counter China's AI efforts. The stated goal of both these competing groups is to provide global governance, including building guardrails and setting…

ContinueIs Rapid Electrification Stimulating Pakistan's Economy?

Pakistan's electricity demand has soared 21% in just two years. Rapid electrification is positively impacting all sectors of Pakistan's economy. thanks to growing deployment of distributed solar, estimated at 38 GW as of June, 2025. In 2025, 44% of solar deployment was residential, followed by industry (26%), agriculture (21%) and commercial users (9%). It is stimulating demand for a variety of products ranging from air conditioners and refrigerators to washing machines and…

Continue

© 2026 Created by Riaz Haq.

Powered by

![]()

You need to be a member of PakAlumni Worldwide: The Global Social Network to add comments!

Join PakAlumni Worldwide: The Global Social Network