PakAlumni Worldwide: The Global Social Network

The Global Social Network

Raast Aims to Create Pakistan's Unified Digital Payments Infrastructure

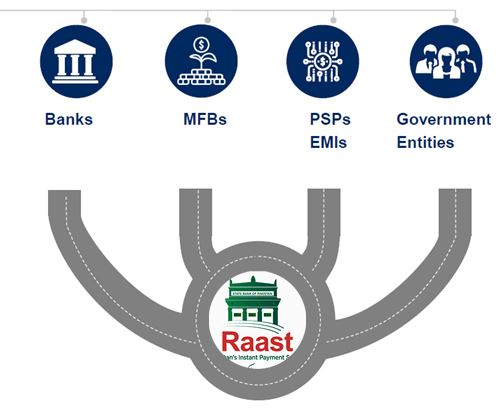

Pakistan's central bankers have taken the plunge into the world of digital payments with their own offering: Raast. It aims to create an instant low-cost payment system that can seamlessly and securely connect government entities, a variety of banks, including microfinance banks (MFBs), electronic money institutions (EMIs) and State Bank authorized payment service providers (PSPs) like 1Link and NIFT which may choose to take advantage of it. Currency and coins in circulation account for about 43% of Pakistan's total money supply. The introduction of Raast is part of the government's effort to modernize and document the nation's cash-based informal economy. Undocumented economy poses a serious threat to the country because it creates opportunities for criminal activities and tax evasion. Digital financial services will also promote e-commerce in Pakistan.

|

| Raast Digital Payment System. Source: State Bank of Pakistan |

Raast Digital Payments:

Raast is a system of digital payment infrastructure. It is essentially a pipe that is intended to connect government and financial institutions with consumers and merchants with each other to process payments instantly at very low cost.

Raast will be boosted by Pakistan government's decision to use it to pay salaries, pensions and pay welfare recipients under Benazir Income Support and Ehsaas Emergency Cash programs.

State Bank of Pakistan intends to demonstrate Raast's usefulness by first processing government payments to individuals, including government employees and Ehsaas welfare beneficiaries, before expanding it for business applications. SBP’s plan is to start person-to-person (P2P) payments using just the phone numbers in Q3/2021 and then bring merchants on board with QR codes by Q1/2022.

Pakistan's Sadia Zahidi Leads WEF Gender Equity Effort

Brothers From Rural Pakistan Teaching AI to American High Schoolers

Pakistan's Computer Services Exports Jump 26% Amid Coronavirus Lock...

Pakistan Gig Economy Among World's Fastest Growing

Digital BRI and 5G in Pakistan

Pakistan's Demographic Dividend

Pakistan EdTech and FinTech Startups

State Bank Targets Fully Digital Economy in Pakistan

Campaign of Fear Against CPEC

Fintech Revolution in Pakistan

E-Commerce in Pakistan

The Other 99% of the Pakistan Story

FMCG Boom in Pakistan

Belt Road Forum 2019

Fiber Network Growth in Pakistan

Riaz Haq's Youtube Channel

Views: 958

-

Comment by Riaz Haq on December 23, 2022 at 5:01pm

-

Mobile banking doubles, internet banking grows by 51.7% in FY2021-22

As internet banking, POS, and eCommerce transactions post strong growth, the digital payments ecosystem is picking up steam

https://profit.pakistantoday.com.pk/2022/12/23/mobile-banking-doubl...

https://www.sbp.org.pk/PS/PDF/FiscalYear-2021-22.pdf

The overall number of payment cards, however, decreased during the year, from 45.9 million in 2020-21 to 42.4 million in 2021-22.

Bring in the fintech

According to the State Bank’s annual report, the four fully licensed EMIs (electronic money institution); Sadapay, Nayapay, Finja and CMPECC, combined had 262,558 total active accounts and 514,961 payment cards issued to their customers. Last year’s numbers on EMIs were not available for a comparison on how these numbers have grown.

The SBP has in the past has often emphasised on the potential fintech can play to boost digital payments and financial inclusion.

During his speech at the Institute of Banking Pakistan Annual Award Ceremony, Jameel Ahmad, Governor SBP stressed on the need for banks to revisit their traditional approach to service delivery and adapt quickly as digitalization shifts the balance of power from banks to tech savvy entities, hinting at the growing trend in fintech.

“Leveraging digital technology is essential not only to promote financial inclusion, but also to ensure that the industry keeps pace with emerging global trends,” opined Ahmed.

Speaking on the importance of technology, Ahmad quotes M-Pesa, a Kenyan fintech. “An often-cited success story is that of M-Pesa in Kenya, where it single-handedly drove mobile financial services availability and successfully raised financial services access in Kenya. “

Ahmad pointed out that a number of factors already exist in Pakistan that can help drive digital financial innovation and proliferation of a tech-based financial ecosystem. He pointed out that the nation has a fully functional digital ID system, ubiquity of mobile devices, penetration of mobile and broadband services, availability of faster payment rails, remote account opening process, and facilitative regulatory environment for enabling the entry of non-bank entities into the financial arena.

The Central Banker also points out that while fintech has brought competition, it also presents the sector with an opportunity to create synergies and mutually beneficial partnerships.

“Banks and Fintechs can partner with each other to provide innovative products for customers that are otherwise not viable on a standalone basis. For banks, such partnerships can help with penetration in untapped segments like retail businesses and Micro and Small Medium Enterprises, yielding beneficial outcomes for all stakeholders,” he said.

Encouraging the banks that are yet to make consistent and sustained moves toward technological transformation, Ahmad told them to make use of the digital bank frameworks and the instant payment system, RAAST, to position themselves for the future.

-

-

SBP

@StateBank_Pak

#SBP journey of digitization achieves another significant milestone, as the Raast Person to Person (P2P) payments cross PKR 1 trillion in a span of just 11 months. SBP thanks all stakeholders who are part of this journey and especially the customers for using #Raast.https://twitter.com/StateBank_Pak/status/1616098619668439043?s=20&a...

-

-

#DigitalIndia: #Digital #Payments, Even for a 10-Cent Chai, Are Colossal in Scale. #India’s homegrown payment system has remade #commerce, pulled millions into formal #economy. Digital IDs ease creation of bank accounts, the basis of UPI instant payment system https://www.nytimes.com/2023/03/01/business/india-digital-payments-...

The little QR code is ubiquitous across India’s vastness.

You find it pasted on a tree next to a roadside barber, propped on the pile of embroidery sold by female weavers, sticking out of a mound of freshly roasted peanuts on a snack cart. A beachside performer in Mumbai places it on his donations can before beginning his robot act; a Delhi beggar flashes it through your car’s window when you plead that you have no cash.

The codes connect hundreds of millions of people in an instant payment system that has revolutionized Indian commerce. Billions of mobile app transactions — a volume dwarfing anything in the West — course each month through a homegrown digital network that has made business easier and brought large numbers of Indians into the formal economy.

The scan-and-pay system is one pillar of what the country’s prime minister, Narendra Modi, has championed as “digital public infrastructure,” with a foundation laid by the government. It has made daily life more convenient, expanded banking services like credit and savings to millions more Indians, and extended the reach of government programs and tax collection.

With this network, India has shown on a previously unseen scale how rapid technological innovation can have a leapfrog effect for developing nations, spurring economic growth even as physical infrastructure lags. It is a public-private model that India wants to export as it fashions itself as an incubator of ideas that can lift up the world’s poorer nations.

“Our digital payments ecosystem has been developed as a free public good,” Mr. Modi said on Friday to finance ministers from the Group of 20, which India is hosting this year. “This has radically transformed governance, financial inclusion and ease of living in India.”

In simple terms, Indian officials describe the digital infrastructure as a set of “rail tracks,” laid by the government, on top of which innovation can happen at low cost.

At its heart has been a robust campaign to deliver every citizen a unique identification number, called the Aadhaar. The initiative, begun in 2009 under Mr. Modi’s predecessor, Manmohan Singh, was pushed forward by Mr. Modi after overcoming years of legal challenges over privacy concerns.

The government says about 99 percent of adults now have a biometric identification number, with more than 1.3 billion IDs issued in all.

Nandan Nilekani, a co-founder of the information technology giant Infosys who has been involved in India’s digital identification efforts since their early days, said the country could make a technological leap because it had little legacy digital infrastructure in place. “India was able to develop afresh with a clean slate,” he said.

-

-

Financial inclusion in Pakistan increases to 30% - Profit by Pakistan Today

https://profit.pakistantoday.com.pk/2023/02/08/financial-inclusion-...

https://portal.karandaaz.com.pk/dataset/financial-digital-inclusion...

KARACHI: Financial inclusion in Pakistan has increased by 9 basis points from 2020 to 2022 and women’s access, specifically has hit a double-digit percentage for the first time, as recorded by a survey conducted by Karandaaz Pakistan.

As defined by the World Bank, “financial inclusion means that individuals and businesses have access to useful and affordable financial products and services that meet their needs – transactions, payments, savings, credit and insurance – delivered in a responsible and sustainable way.” This means conducting transactions through banks, mobile money and fintech.

The Karandaaz Financial Inclusion Survey (K-FIS) measures the percentage of adults above the age of 15 who report having at least one account in their name with an institution that offers a full range of financial services that is also documented by the government of Pakistan.

Following a significant jump in financial inclusion between 2017 and 2020, K-FIS recorded a substantial rise in the level of financial inclusion from 21% in 2020 to 30% of adults in 2022. Registered mobile money users more than doubled with an increase from 9% to 19%, while registered bank users also increased by 4 basis points over the same period.

By region, Islamabad Capital Territory (ICT) recorded the highest level of financial inclusion at 45%, followed by Gilgit Baltistan at 35% and Azad Jammu & Kashmir at 34%.

Looking at the division by gender, male registration accounted for the bulk of financial account registrations in 2022 with 47% having at least one registered financial account. Comparatively, only 13% of women are recorded to have at least one registered financial account. Although women’s percentage accounts for less than half of their male counterparts, the financial account registration for women has reached double digits for the first time.

Overall, the largest increase was seen in mobile money wallet users, as active usage increased from 8% in 2020 to 16% in 2022. Active usage also saw an increase in bank account holders, indicating an increase from 12% in 2020 to 14% in 2022.

Addressing the webinar held by Karandaaz Pakistan on February 7, 2023, Noor Ahmed, Director of the Agri Finance and Financial Inclusion Department of the State Bank of Pakistan (SBP) said, “Over the years, there has been significant progress on financial inclusion. Key initiatives such as RAAST have been transformative in furthering the inclusion of the marginalised.”

Karandaaz Pakistan is a not-for-profit special-purpose vehicle set up under Section 42 in August 2014. The company is the implementation partner of the Enterprise and Asset Growth Programme (EAGR) and Sustainable Energy and Economic Development (SEED) programme of the UK’s Foreign, Commonwealth & Development Office (FCDO).

-

-

The Challenges of Pakistan’s Digital Banking Reality - Aurora

https://aurora.dawn.com/news/1144694

The much-anticipated wait for the coveted digital banking licenses from the State Bank of Pakistan (SBP) is finally over. The five recipients (out of 20) must now lead the way and showcase how effective digitally enabled banking can be in solving the financial inclusion conundrum (digital and otherwise) of the unserved and underserved segments of Pakistan.

They will also be expected to possess/create better digital strategies, architectures and approaches to benefit the financial services industry, and given that no local bank got the go-ahead (at least in this round), it will be interesting to see how many of those revert to applying again or opting for Plan B and protect their market share by digitally enhancing themselves, re-evaluating their HR strategies, aligning the right percentage points for the right products and services, taking a deeper look at their digital architecture, and renewing their go-to market approach.

Traditionally, leading digital outlets are mapped internally and externally and have the right processes and tools to make digital channels available for bank customers and their various divisions. They also will have to learn from fintechs (or partner with them) to enable new digital customer journeys and user experiences by leveraging automated/paperless workflows and environments for better acquisition, retention and growth. Unfortunately, in the Pakistani context, success in digital banking (thus far and for most) equates to their banking apps on mobiles, where one can pay bills or another. Beyond this, for all other banking needs, the parameters of real digital banking success are still hard to define, given that the public still relies on hard cash rather than digits on a screen.

So, who are these digital banking leaders? In my view, out of 33 operating banks, six have demonstrated at the very least a decent digital vision and the ability to lead, if not total prowess on their strategies, customer focus, and the value of their services through innovative channels. Bank Alfalah, HBL and Meezan Bank seem to be the clear market leaders, followed by Allied Bank, Standard Chartered Pakistan and United Bank. Another three to four are trying to up their game to stay digitally relevant. Time will tell if they succeed.

The top ones are better placed than the others in terms of digital capability, governance structures, and professional decision-making (as opposed to seth or state-driven) and have an overarching ‘doer’ attitude that is reflected in their products/services. They also have stronger working digital partnerships with the SBP; they try out new, technologically advanced techniques and comply with the requisite investments in digital and hire on mandated appointments to advise on, and lead, IT initiatives. Their leveraging of the Covid-19 pandemic as an opportunity to explore new digital methods, address customer needs and focus on banking initiatives such as Raast and Roshan Digital Accounts are also commendable.

The remaining digital laggards seem to have their own reasons for doing the bare minimum on this front. For them, going digital (in the true sense) is time-consuming, expensive and the ROI of effort versus the reward does not make strategic sense given their lack of experience in monetising digital channels. Their best option will be to opt for profitability through traditional branch deposits, knowing fully well that cost centre models that typically flow down from branch banking are the most expensive, followed by ATMs – digital channels being the cheapest.

-

-

The Challenges of Pakistan’s Digital Banking Reality - Aurora

https://aurora.dawn.com/news/1144694

In their quest to go completely digital, banks are also struggling in the following areas.

Customer Ownership: In the digital sense, customer journeys stemming from apps/digital channels that leverage the banking services and products available to them will be a challenge. And since HR structuring is done in an old-fashioned way, the back-end reconciliation is often not only an operational challenge, it becomes an office politics one.

Parallel Digital Structures: Many banks have opted for a parallel albeit small(er) digital infrastructure to test the digital waters (perhaps they were advised to do this). The jury is still out on this approach because many of them preferred to digitally transform themselves completely and achieve overall digital excellence, rather than do it for one division and then connect others to it. This often creates a caste system within banks, which can also be a cultural challenge to solve for the leadership.

Skill Sets and Talent: Digital thinking at banks is often led by a tech-savvy board member, a digital banking leader and a CIO – all of whom are not always in sync, partly because they rose in different working environments and sectors. CIOs have risen in the ‘networking’ or ‘application’ route and are a non-business-savvy tech resource at best. Digital banking leaders are typically non-bankers and the board member is a foreigner (no formal board-level technology governance education exists in Pakistan) and is not, therefore, always up to speed in terms of Pakistan knowledge. This challenge exists across the board, especially because digital talent is still being cultivated (including junior ranks) and it often opts for start-ups and freelancing so that banks are even more challenged when it comes to attracting/retaining top talent.

Tech Architecture: Digital prowess requires stellar digital architectures, and to my knowledge, none of the banks has conducted a deep forensic audit of their existing tech stacks in order to uncover vulnerabilities and test the strengths on which the digital architecture is to stand. Untested architectures can be exposed and insecure and as dimensions of digital apps/tools/security are added to the volumes of transactions and data that a modern digital bank enables, they can fall (and fail).

Tech Tools: T24 by Temenos seems to be a core banking darling among CIOs. Enterprise Resource Planning exists for accounting and finance mechanisms, and CRM is widely missing as they don’t see the value somehow (shocking). Furthermore, internet banking architectures are different from those of mobile banking and back-end integration on a single connected stack for efficiency is missing. The SBP’s latest framework to outsource to cloud service providers is a welcome gesture, but to leverage it, banks will have to rethink their architecture and stop relying on band-aid approaches.

What next? Regardless of how the new digital licensees do, local banks should transform customer journeys at the branch level by digitising end-to-end digital loan disbursements/underwriting and all human/paper-intensive areas. This will involve constant upgrading of their digital vision, automating processes/workflows, focusing on customer centricity, upgrading the tech stacks, and integrating and mimicking digital channels with traditional branches. There will also have to be a meticulous focus on employee training in new-era banking, data gathering, intelligent decision-making and coming up with out-of-the-box customer and culturally relevant products that Pakistanis need to survive and grow.

Javaid Iqbal is CCO (and Member and Executive Director), Special Technology Zones Authority, Cabinet Division, Government of Pakistan. The thoughts reflected in this article are entirely his own and do not represent the views of the government. He can be followed on http://linkedin.com/in/jiqbal and @jdiq

-

-

Navigating NADRA's Journey Towards Greater Inclusion and Digital Transformation: An Outsider's Perspective

Atyab Tahir

https://www.linkedin.com/pulse/navigating-nadras-journey-towards-gr...

3. Leverage RAAST:

NADRA's symbiosis with #RAAST, Pakistan's instant payment system, can redefine how government benefits reach citizens. Mirroring India's Aadhaar Enabled Payment System (AEPS) and Kenya's M-Pesa, this system can enhance the speed, security, and convenience of government-to-person (G2P) payments. #DigitalPayments #NADRA #RAAST

----------

A conversation with a friend recently propelled me towards an intriguing exploration. He asked for my perspective on enhancing the role of Pakistan's National Database and Registration Authority (NADRA), akin to India's Aadhaar system. That thought-provoking question led to the genesis of this article.

NADRA, since its inception in the 90s, has greatly influenced the landscape of data collection, storage, and usage in Pakistan. Representing one of the world's most comprehensive citizenship databases, it has facilitated various administrative and governance processes, from issuing the Computerized National Identity Card (CNIC) to passport services and beyond.

In the global #DigitalRevolution era, the Aadhaar system shines as a beacon of #PublicService transformation and inclusivity, urging us to recognize NADRA's transformative potential. With its comprehensive reach and capabilities, NADRA is poised to act as a significant change catalyst, steering us towards a more #DigitallyInclusive Pakistan.

1. Interoperability and Integration:

NADRA must facilitate seamless integration with other government systems, across national to local levels. Taking a leaf from Estonia's X-Road platform, a secure data exchange layer connecting multiple databases, NADRA can contribute to an efficient, citizen-centric administrative system. #DigitalIntegration

2. Financial Inclusion:

Aadhaar's success is tied closely to promoting #FinancialInclusion. NADRA, too, can kindle such progress in Pakistan. Facilitating default bank accounts linked to CNICs, NADRA can launch a financial revolution, integrating the unbanked into the mainstream financial realm.

Brazil used its citizen registry to deliver emergency COVID-19 aid to 67 million Brazilians, reflecting how such an integrated approach can create real impact. Similarly, NADRA, in sync with financial institutions, could provide Pakistani citizens with much-needed financial assistance. By leveraging its extensive database, NADRA can further aid in credit scoring and risk assessment for loans, extending credit facilities to previously underserved segments. #FinancialInclusion #DigitalBanking

3. Leverage RAAST:

NADRA's symbiosis with #RAAST, Pakistan's instant payment system, can redefine how government benefits reach citizens. Mirroring India's Aadhaar Enabled Payment System (AEPS) and Kenya's M-Pesa, this system can enhance the speed, security, and convenience of government-to-person (G2P) payments. #DigitalPayments #NADRA #RAAST

4. Privacy Protection:

Robust data protection measures are paramount as NADRA expands its influence. Fostering public trust requires a transparent mechanism for data access and sharing, coupled with guaranteed data encryption. The European Union's GDPR provides a robust framework for such an endeavor. #DataProtection

-

-

Pakistan's NayaPay Partners With Alipay+, A Cross-Border Digital Payments Service Operated By Ant International | Crowdfund Insider

https://www.crowdfundinsider.com/2024/01/220805-pakistans-nayapay-p...

NayaPay, a financial platform, has partnered with Alipay+, a cross-border digital payments and marketing platform operated by Ant International.

The collaboration between NayaPay and Alipay+ is set “to make a significant impact by deploying QR codes compatible with both RAAST and Alipay+ payment partners, including e-wallets and bank apps, thereby enhancing incoming foreign exchange flows and integrating the cashless payment systems of global markets and Pakistan.”

This strategic alliance is specifically designed “to streamline digital payments, tackling prevalent issues such as limited interoperability and elevated transaction costs.”

Through this partnership, NayaPay is well-positioned to “provide Pakistani businesses of all sizes, particularly SMEs, with a seamless connection to more than 25 Alipay+ global payment partners, which reaches a total of more than 1.5 billion consumer accounts, in addition to RAAST.”

This initiative ensures that transactions “are not only efficient but also secure, marking a major step forward in the digitization of commerce in Pakistan.”

Furthermore, this partnership is anticipated “to empower businesses in Pakistan to transact seamlessly with global visitors through a low-cost and fast payment system. This will foster documented and cashless trade and tourism between the two countries.”

This initiative is in line with the State Bank of Pakistan’s vision “for the nation’s economic advancement and digital evolution, setting a new benchmark in the region’s financial sector.”

As noted in the update, Alipay+ is “a suite of cross-border digital payment, marketing and digitalization solutions that help connect global merchants to consumers.”

Consumers enjoy seamless payment and “a broad choice of deals using their preferred payment methods while traveling abroad. Small and medium-sized businesses may use Alipay+ digital tools to enhance efficiency and achieve omni-channel growth.”

As covered in early 2022, Pakistan’s NayaPay Pvt. has reportedly acquired $13 million in early-stage capital as it aims to onboard consumers who an underbanked or financially underserved.

The Karachi-headquartered Fintech firm’s seed round has been led by Zayn Capital, MSA Novo and Silicon Valley’s early-stage investor Graph Ventures, CEO Danish Lakhani confirmed (in statements shared with Bloomberg).

NayaPay became the first startup to provide financial services after acquiring an operational license from the State Bank of Pakistan back in August 2021. The Fintech company’s chat-based payments app launched by focusing on freelancer workers and students.

Comment

- ‹ Previous

- 1

- …

- 3

- 4

- 5

- Next ›

Twitter Feed

Live Traffic Feed

Sponsored Links

South Asia Investor Review

Investor Information Blog

Haq's Musings

Riaz Haq's Current Affairs Blog

Please Bookmark This Page!

Blog Posts

Pakistani Student Enrollment in US Universities Hits All Time High

Pakistani student enrollment in America's institutions of higher learning rose 16% last year, outpacing the record 12% growth in the number of international students hosted by the country. This puts Pakistan among eight sources in the top 20 countries with the largest increases in US enrollment. India saw the biggest increase at 35%, followed by Ghana 32%, Bangladesh and…

ContinuePosted by Riaz Haq on April 1, 2024 at 5:00pm

Agriculture, Caste, Religion and Happiness in South Asia

Pakistan's agriculture sector GDP grew at a rate of 5.2% in the October-December 2023 quarter, according to the government figures. This is a rare bright spot in the overall national economy that showed just 1% growth during the quarter. Strong performance of the farm sector gives the much needed boost for about …

ContinuePosted by Riaz Haq on March 29, 2024 at 8:00pm

© 2024 Created by Riaz Haq.

Powered by

![]()

You need to be a member of PakAlumni Worldwide: The Global Social Network to add comments!

Join PakAlumni Worldwide: The Global Social Network