PakAlumni Worldwide: The Global Social Network

The Global Social Network

Digital Transactions in Pakistan Soared 30% to $500 Billion in Fiscal Year 2020-21

Digital transactions in Pakistan soared 31.1% to Rs. 88 trillion or $500 Billion in fiscal year 2020-21, according to the nation's top central banker. “If the figure is $500 billion now, you can imagine the pace at which we are digitizing,” said Dr. Baqir Raza, Governor of the State Bank of Pakistan, adding that those transactions showed a year-on-year growth of 30.6% in volume and 31.1% in value. The nation's central bank also reported that the large-value payments segment, known as Real-time Inter-Bank Settlement Mechanism (PRISM), saw growth of 60% by volume and 12.8% by value to Rs. 444.6 trillion or $2.5 trillion in FY 2020-21. There are several factors driving rapid shift to digital technology, including expanding digital infrastructure, new technologies and the government's efforts to document Pakistan's huge undocumented economy. Grey-listing of Pakistan by the Financial Action Task Force (FATF) has also played a role.

|

| Internet & Mobile Banking in Pakistan. Source: SBP |

Digital Transactions Growth:

Growth in digital transactions was led by major uptake in mobile banking (29% increase in the number of users and 133.6% and 178.7% hike in volume and value, respectively) and internet banking (32% increase in the number of users and 65.1% and 91.7% up in volume and value, respectively), according to the State Bank of Pakistan. “If the figure is $500 billion now, you can imagine the pace at which we are digitizing,” said Dr. Baqir Raza, the head of Pakistan's central bank.“Therefore, there is a huge potential for enhancing financial inclusion,” he added.

|

| E-Banking in Pakistan. Source: Dawn |

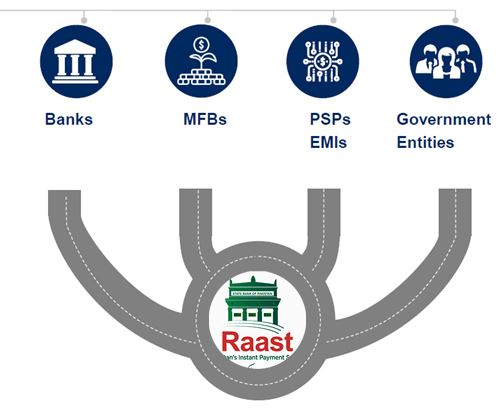

Pakistan's central bankers have taken the plunge into the world of digital payments with their own offering: Raast. It aims to create an instant low-cost payment system that can seamlessly and securely connect government entities, a variety of banks, including microfinance banks (MFBs), electronic money institutions (EMIs) and State Bank authorized payment service providers (PSPs) like 1Link and NIFT which may choose to take advantage of it. Currency and coins in circulation account for about 43% of Pakistan's total money supply. The introduction of Raast is part of the government's effort to modernize and document the nation's cash-based informal economy. Undocumented economy poses a serious threat to the country because it creates opportunities for criminal activities and tax evasion. Digital financial services will also promote e-commerce in Pakistan.

|

| Raast Digital Payment System. Source: State Bank of Pakistan |

Raast Digital Payments:

Raast is a system of digital payment infrastructure. It is essentially a pipe that is intended to connect government and financial institutions with consumers and merchants with each other to process payments instantly at very low cost.

Raast will be boosted by Pakistan government's decision to use it to pay salaries, pensions and pay welfare recipients under Benazir Income Support and Ehsaas Emergency Cash programs.

State Bank of Pakistan intends to demonstrate Raast's usefulness by first processing government payments to individuals, including government employees and Ehsaas welfare beneficiaries, before expanding it for business applications. SBP’s plan is to start person-to-person (P2P) payments using just the phone numbers in Q3/2021 and then bring merchants on board with QR codes by Q1/2022.

Pakistan's Undocumented Entrepreneurs

Brothers From Rural Pakistan Teaching AI to American High Schoolers

Pakistan's Computer Services Exports Jump 26% Amid Coronavirus Lock...

Pakistan Gig Economy Among World's Fastest Growing

Digital BRI and 5G in Pakistan

Pakistan's Demographic Dividend

Pakistan EdTech and FinTech Startups

State Bank Targets Fully Digital Economy in Pakistan

Campaign of Fear Against CPEC

Fintech Revolution in Pakistan

E-Commerce in Pakistan

The Other 99% of the Pakistan Story

FMCG Boom in Pakistan

Belt Road Forum 2019

Fiber Network Growth in Pakistan

Riaz Haq's Youtube Channel

Views: 621

-

Comment by Riaz Haq on May 14, 2022 at 7:14pm

-

The Indian economy is being rewired. The opportunity is immense

And so are the stakes

https://www.economist.com/leaders/2022/05/13/the-indian-economy-is-...

As the country emerges from the pandemic, however, a new pattern of growth is visible. It is unlike anything you have seen before. An indigenous tech effort is key. As the cost of technology has dropped, India has rolled out a national “tech stack”: a set of state-sponsored digital services that link ordinary Indians with an electronic identity, payments and tax systems, and bank accounts. The rapid adoption of these platforms is forcing a vast, inefficient, informal cash economy into the 21st century. It has turbocharged the world’s third-largest startup scene after America’s and China’s.

Alongside that, global trends are creating bigger business clusters. The it-services industry has doubled in size in a decade, helped by the cloud and a worldwide shortage of software workers. Where else can Western firms find half a million new engineers a year? There is a renewable-energy investment spree: India ranks third for solar installations and is pioneering green hydrogen. As firms everywhere reconfigure supply chains to lessen their reliance on China, India’s attractions as a manufacturing location have risen, helped by a $26bn subsidy scheme. Western governments are keen to forge defence and technology links. India has also found a workaround to redistribute more to ordinary folk who vote but rarely see immediate gains from economic reforms: a direct, real-time, digital welfare system that in 36 months has paid $200bn to about 950m people.

-

-

Pakistan to launch digital ID wallet this year

By Daniel Tost - March 8, 2022, 6:19 pm

https://www.globalgovernmentfintech.com/pakistan-to-launch-digital-...

Pakistan’s National Database and Registration Authority (NADRA) is planning to roll out a digital identity wallet later this year in a move that will end the need for physical ID.

NADRA is tasked with digitising all citizen data in the country, which – with more than 220 million citizens – is the fifth biggest in the world in terms of population.

As part of a digital push aimed at generating benefits including greater financial inclusion, the authority is working on a significant evolution of the existing ‘Pak-ID’ smartphone app – which was itself only introduced seven months ago, the authority’s chairman Tariq Malik told Pakistani media Dawn.

Launched last September, Pak-ID allows citizens to apply for a physical ID card remotely by using their Android or iOS device to scan documents and biometric data including their fingerprints and take a picture to verify their identity. When it was introduced, NADRA proclaimed that Pakistan had become ‘the first country in the world to introduce ID technology’. Two weeks later, the authority launched a similar biometric verification service for the banking and payments industry. With five banks initially participating, the service enables customers to open bank accounts and undertake biometric authenticated financial transactions using a mobile-phone camera.

Hailing Pak-ID’s debut, prime minister Imran Khan called the app “a revolutionary step in providing convenience, especially to overseas Pakistanis”. It seems these expats have at least partly driven the decision to launch the digital identity wallet by updating the Pak-ID app. “In a short span, 75,000 overseas Pakistanis have processed their national identity cards from the comfort of their homes by using the app,” Malik told Dawn. “With successful testing on 75,000 overseas Pakistanis, NADRA will go for a digital wallet.”

The wallet would be “a leap forward putting an end to the conventional physical ID” and is to be made available “later this year”, Malik said. “The digital dividends of such technology innovation will yield positive results in contactless banking, financial inclusion, ease of doing business and e-governance initiatives by offering remote identification and e-KYC [know-your-customer procedures].”

-

-

Pakistan to launch digital ID wallet this year

By Daniel Tost - March 8, 2022, 6:19 pm

https://www.globalgovernmentfintech.com/pakistan-to-launch-digital-...

Focus on unregistered citizens

As of January, 96 per cent of Pakistan’s adult (above 18) population, have a Computerised National Identity Card (CNIC), according to Islamabad-headquartered NADRA. Pakistan started rolling out its Smart National Identity Card (SNIC) in 2012 in a programme overseen by NADRA and aimed at replacing CNICs. Currently, both types of cards remain valid.

Recently, NADRA has focused on unregistered individuals (citizens without an identity card) by creating an ‘Inclusive Registration Department’. Its aim is to enhance registration, especially for women, minorities, transgender and unregistered persons. The agency targeted 80 districts with a gender gap of more than 10 per cent in registration figures. Eighteen female-only NADRA centres were opened to overcome socio-cultural barriers of women cautious about dealing with male staff. Additionally, 262 mobile registration vans and 80 ‘ManPack’ mobile units have been deployed countrywide for people living in remote areas or senior citizens who may struggle to travel. In total there are more than 700 registration centres operating countrywide and in all 154 districts of Pakistan. According to a NADRA press notice issued last month, the gender gap has been reduced by 40 per cent in targeted districts.

NADRA says it holds the largest biometric database of citizens in the world. The security of such a stock of citizen data is clearly important but the authority states that its SNIC is equipped with 36 security features, using a layering system to safeguard sensitive information.

Principles for interoperable ID

Pakistan’s move comes against the international backdrop of high-level principles to support the development of mutually recognised and interoperable digital ID systems and infrastructure having been drafted by a working group on digital identity comprising representatives from eight countries.

The 11 principles call for digital ID infrastructure to be open; transparent; reusable; user-centric; inclusive and accessible; multilingual; secure and private; technologically neutral and compatible with data portability; administratively simple; able to preserve information; and effective and efficient.

In its report, the Digital Identity Working Group (DIWG) said its goal is to enhance trade agreements and to ‘facilitate economic recovery from Covid-19, for example to support the opening of domestic and international borders’.

Established in 2020, DIWG comprises Australia, Canada, Finland, Israel, New Zealand, Singapore, the Netherlands and the UK. It is chaired by Australia’s Digital Transformation Agency.

-

-

SBP

@StateBank_Pak

Another milestone achieved by #SBP in the journey of digitization, as number of #Raast IDs registration crosses 10 million mark since its launch in Feb22. Aggregated value of Person to Person (P2P) Transactions using #Raast system by customers crosses Rs36bn.https://twitter.com/StateBank_Pak/status/1526174517910986755?s=20&a...

-

-

Informal Savings in Pakistan

https://www.dawn.com/news/1725956

According to research by Oraan, around 41pc Pakistanis saved via committees (or Rosca), whereas Karandaaz puts that figure at 34pc. Assuming the informal economy accounts for roughly 30pc, as suggested by research from the Pakistan Institute of Developing Economics, it translates into annual committees of Rs4 trillion at base prices, using conservative inputs.

While this back-of-the-envelope calculation is far from scientific, it helps contextualise how big the informal savings market really is. Everyone from a widow looking to save up for her children’s education to young adults trying to save up for their marriage, committees are what they turn to.

This phenomenon is not exclusive to Pakistan. According to a note by Middle East Venture Partners (one of the investors in Bykea), “the global market is largely untapped and ripe for disruption with 2.4 billion people using money circles through traditional channels.”

They recently participated in the Egyptian digital committees’ startup MoneyFellows’ $31m Series B.

Apart from the traditional financial institutions’ general apathy towards the customer, committees appeal to an average Pakistani for several reasons: they are a community-based instrument with some level of flexibility and there is no interest involved.

Most importantly, it helps them manage cash flow better due to habitual change. For women, the product enjoys particular popularity since the former financial services are largely inaccessible.

However, since committees are primarily cash-based with virtually no money trail involved, it poses massive risks, as we saw recently when a girl, Sidra Humaid, who ran a network of committees through social media, defaulted on Rs420m of payments.

----

Even beyond this, committees have flaws by design, only amplified by Pakistan’s macros. For instance, the person receiving the first lump sum amount will always be at an advantage since their instalments in the subsequent months would be worth less due to both inflation and rupee depreciation. The recipient of the last payment would see the amount’s purchasing power eroded substantially by the time they get it.

Moreover, due to the community-based nature of the product, the risk of network defaulting is higher as people of usually similar risk profiles would be pooling in their money.

For example, if employees from an organisation have running office committees, delayed salaries or layoffs within the organisation would lead to a bad equilibrium, creating losses for the rest of the group, often resulting in default.

However, there are ways to address some of those challenges. First of all, to (partially) protect your lump sum from depreciation or devaluation, you can enter a committee with a duration of up to 10 months. Given Pakistan’s macros of late, you’d still lose money in real terms but to be fair, that’d most likely be the case in any other instrument as well, including the risk-free government papers.

In fact, contrary to popular perception, there are certain ways to further alleviate the inflation problem. Digital committees have an option of gamifying the experience by rewarding good payment behaviour through loyalty programs and/or brand partnerships to provide discounts on utilities-based services and products.

Secondly, digital committees help create a trail of money which, coupled with a centralised authority (the platform itself), brings in accountability and recourse in the event of a default. The receipt and/or ledger helps with basic accounting in committees creating transparency for people within the group.

The third benefit of digital committees is the security factor. The participant has to go through a know-your-customer and credit check process to make sure there is no fraudulent behaviour that could negatively impact the group, along with the participant’s ability and willingness to pay to create an overall environment for responsible finance.

Comment

- ‹ Previous

- 1

- 2

- Next ›

Twitter Feed

Live Traffic Feed

Sponsored Links

South Asia Investor Review

Investor Information Blog

Haq's Musings

Riaz Haq's Current Affairs Blog

Please Bookmark This Page!

Blog Posts

Is the India Growth Story Over?

In a television speech to the nation, Indian Prime Minister Narendra Modi urged his people to make sacrifices by spending less on fuel, fertilizer, and travel. He also asked them not to buy gold for a year. “To save foreign exchange, we must accept the challenge of patriotism,” he said. It appears that India's problems do not just stem from the effects of the US-Iran war; India's problems started well before that. Flight of foreign capital has put the Indian currency under tremendous…

ContinuePakistan's New Infrastructure Investments and Trade Routes

Pakistan has recently launched 5G wireless service in multiple cities and closed financing on the 306 kilometer 6-lane Sukkur-Hyderabad M6 motorway. In addition, Pakistan is seeing significant increase in the utilization of its Gwadar and Karachi ports after the closure of the Strait of Hormuz due to the US-Iran war. This will help open the trade routes from Pakistan to Central Asia via Iran, bypassing unstable Afghanistan. It has the potential to eventually make Pakistan a major…

ContinuePosted by Riaz Haq on May 4, 2026 at 5:00pm — 4 Comments

© 2026 Created by Riaz Haq.

Powered by

![]()

You need to be a member of PakAlumni Worldwide: The Global Social Network to add comments!

Join PakAlumni Worldwide: The Global Social Network